Some insights from IAG

IAG, or the International Airlines Group, is the the parent of Aer Lingus, British Airways and Iberia. In my university, we were lucky enough to have their CEO, Willie Walsh, speak to us before Christmas.

IAG, or the International Airlines Group, is the the parent of Aer Lingus, British Airways and Iberia. In my university, we were lucky enough to have their CEO, Willie Walsh, speak to us before Christmas.

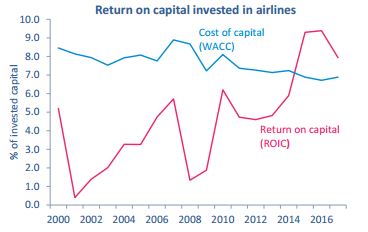

Some things he mentioned are relevant to this blog, and of course interesting. One thing Mr Walsh noted was how only in recent years has the airline sector actually made a return on capital. This must be attributable in some way to a focus on cost by the sector in recent years. The chart below from IATA shows what I mean. As you can see, the cost of capital was higher than the return until 2014.

As my last post indicated, a focus on cost and efficiency has been a feature of the airline sector in recent years. To give another example, Mr Walsh cited an example of using two larger aircraft on a route without a loss in passenger capacity. So fuel, crew and capital cost all decrease in such a scenario. In addition, it freed up a slot at London’s Heathrow airport, which can then be used to generate more revenues.

Break even for a vineyard.

I read a nice article in the Financial Times recently on the cost of buying a vineyard. The article is investment focused, but mentions that given costs of production, wine prices and annual sales in bottles, the investment will breakeven in a few years – meaning the investment is recouped. If you have studied management accounting, you’ll be aware this not breakeven in the way you many have learned it – fixed cost/contribution per unit. It is not very different though. In essence, the investment is regarded as a fixed cost, with the contribution per unit being the annual contribution which can be made from sales of wine in a year. It’s not a perfect measure, but a good enough rule of thumb to help make an investment decision.

I read a nice article in the Financial Times recently on the cost of buying a vineyard. The article is investment focused, but mentions that given costs of production, wine prices and annual sales in bottles, the investment will breakeven in a few years – meaning the investment is recouped. If you have studied management accounting, you’ll be aware this not breakeven in the way you many have learned it – fixed cost/contribution per unit. It is not very different though. In essence, the investment is regarded as a fixed cost, with the contribution per unit being the annual contribution which can be made from sales of wine in a year. It’s not a perfect measure, but a good enough rule of thumb to help make an investment decision.

A challenge to Ireland’s banks – I’d love to hear your comments

Image (journal.ie)

To this audience I ask two questions

- do you understand short-term versus long-term? If you do, which applies to your decision-making?

- are there any trained management accountants working in banks? I know there are, so read below if you are one of them.

While driving back from Cork recently, I heard a decent sounding lady with six kids telling a story about how a bank was repossessing the house her family rented – it was the Joe Duffy show on RTE Radio 1. The landlord could not afford the loan repayments it seemed and the bank wanted to sell the house. The family worked, and had sufficient income to pay rent into the future. The husband worked in a state-job, so as secure as you could get. She tried to communicate with the bank, but got a “computer says no” type response from the bank. To me, and I am just a management accountant, not a banking expert I could not see the logic in selling the house. Something instinctively told me taking a longer term view is a better choice.

Based on the information she gave during the radio show, when I reach my home I opened an Excel sheet. I checked the rent the lady might be paying – from daft.ie – and then I started to use the simple PMT function in Excel. I made assumptions that the landlord stopped paying the bank loan based on the original house value in 2010; that the bank would allow the lady to take over the mortgage at the present market value of the house and at the present interest rate. I did not adjust for the time value of money. You can see all my workings at this link:

The total time to do the above calculations was about 20 mins. I admit, Excel is not perfect, and I do not adjust for the time value of money – I don’t think it will make things vastly different. To keep it short, if the bank allowed the lady to take over the house as described above, they would gain to the tune of just under €86,000. Based on my simple calculations, the lady could afford to pay this. So, taking a longer term view, the bank (and by definition it’s shareholders) would benefit compared to ditching the house now.

Some further points on costs. I ignore legal costs, as the bank would have to suffer legal costs on either a sale or re-mortgage. But there is a bigger elephant in the room on costs. The lady would be homeless, someone would have to pay this cost – directly or indirectly, and ultimately the state. If I extrapolate the social costs, what is the family (who seemed decent) became homeless, the family fabric was disturbed and the kids turn to crime in the future. How much would this cost in money terms ?

So back to my questions. The scenario I describe above is being repeat all across Ireland. As a person, and an accountant this annoys me. The view of banks seems to be short-term only, driven by profit only. Now don’t get me wrong, profit is good, it creates jobs and investment. But we must not view profit from a short-term perspective. So, to the bankers, give me an answer to the above questions. If you are a trained management accountant, you should be thinking long-term, and if not, don’t think you cannot fail by taking short-term views. As you know banks have failed, as the leading image here should remind you.

Another cost overrun example

Following from my last post, here is another example of costs and design problems -but this one is a real project. A bridge crossing the Bay Area in San Franciso had an original cost estimate of $250, but the final cost was in excess of $6 billion. This occurred for many reasons, bad cost estimates, politics and the length of time involved. Read the article at the link for full detail – it’s a great example of the cost problems associated with infrastructure projects.

Why accountants and designers should work together.

Marketing and design people tend to be very creative, and fair play to them, it’s part of what they are. But design is one thing and actually building or making sometime is tougher – if you have ever built even a standard house you will know what I mean.

Marketing and design people tend to be very creative, and fair play to them, it’s part of what they are. But design is one thing and actually building or making sometime is tougher – if you have ever built even a standard house you will know what I mean.

The one thing I have learned about design of products is to not change the design after you agree it – this typically causes costs to go upwards. If a customer is willing to pay for this great, but that’s usually the exception.

My experience of product design is it is best to involve someone with good management accounting knowledge from the outset. This person need not be an accountant, but must has good knowledge of costs and or processes to build or make the final product. Otherwise big surprises can occur.

Maybe it’s an extreme example but take the main stadium design for the 2020 Olympic Games in Tokyo. According to reports, the cost of the design to be built has doubled to $2 billion since inception. Surely if someone with half decent knowledge of costs working with the designer would have spotted the additional costs.

What is life cycle costing?

You may have seen the typical product life cycle graph in your previous studies (see left). The basic idea is that sales in money and volume increase over time, but gradually tail off as the product comes to the end of its cycle.

You may have seen the typical product life cycle graph in your previous studies (see left). The basic idea is that sales in money and volume increase over time, but gradually tail off as the product comes to the end of its cycle.

When we think of management accounting and product costing, we are generally looking at short-term costs, and not all costs a product may incur over it’s life cycle. For example, there may be advertising costs to boost sales of mature products, costs of product development or even remediation/disposal costs. Life cycle costing include all costs of a product or service from design to end-of-life. All recurring and once-off costs are included over the entire life cycle. These costs can then be compared with expected revenues to determine if a product is profitable or not.

To give you an example, consider the drug development life cycle. It may take many years and cost €billions to bring a drug to market (see here for example, which depicts the process at Bayer), before a single euro in revenue is earned. Then, there are the on-going manufacturing costs. Perhaps the drug has side effects, and needs some improvement during its life. And perhaps as the drug ends its life, there may be costs in dismantling purpose-built manufacturing facilities. Taking all these items (and more no doubt) a drug company can consider if a particular drug is profitable.

Simple graphical reporting

I have written a few posts in the past on the use of infographs to get a key message or statistics across to managers. While on holiday in Germany, I visited a now disused mine and I came across this:

It is a simple graph which shows the injuries at the mine for a nine month period. It does not need much explaining. What strikes me is its utter simplicity – it gets the number across in a clear and simple manner. It should be understood by all staff from managers to workers. It’s on a single page, and drawn manually – probably pre-dates computers.

Building a better income statement – according to McKinsey

McKinsey have a nice web article which highlights the problems with GAAP reporting versus the needs of investors and analysts. The kernel of their article is that financial statements, with some small adjustments, could save investors a lot of re-working of figures. They provide the following example:

Image copyright McKinsey

Two things come to my mind. First, in my first real management accounting job almost 20 years ago now, we prepared an income statement which was not too far away from the one on the right above. And, most management accounting courses would teach students to draw up some kind so similar profit statement – at least separating direct and indirect costs.

Second, the articles does not mention XBRL at all. With tagged data from GAAP financial statements, XBRL could re-draw financial statements in any format. I am not saying all XBRL tags are there to do what McKinsey suggest, but it is certainly possible technically.

You can read the full article at the link below. It is worth a read.

Management accountant’s travelogue – part 3 – to toll or not to toll?

(Photo credit: Wikipedia)

As I drove through France and Spain on my holiday, I thought about the tolls one must pay (on most) motorways. I was thinking how do they set the prices of these tolls? Of course, public infrastructure like motorways is often now financed by a combination of public and private investment. Regardless of the investment type, can you imagine how tricky it is to pitch a price for a motorway toll. If it’s too high, less will use it (M6 Toll in the UK) and costs take much longer to be recouped. Set it too cheap and it floods with traffic, which in turn eventually results in less users, and that equals less money. Should the price be set with future investment and on-going maintenance in mind. Should it be a social good with a very low price – but then where will the money come from for re-investment? Lots of questions here, but I hope you can see a lot of management accounting is behind these decisions. I would imagine getting the initial price correct is the toughest part. Nowadays though, I am sure there are plenty of modelling tools to help toll operators and governments.

Managers should know the numbers

At the end of June this year, Michael O’Leary from Ryanair was his usual self at the Paris Airshow. He let a few jibes fly at almost everyone. He also signed an order with Boeing for new aircraft, worth around $1.5 billion. Plans for future aircraft purchase were mentioned too and O’Leary compared two possible aircraft – one from Boeing and one from Airbus. While he suggested both were similar aircraft, the Boeing has 9 more seats and he said ‘that’s worth a million bucks’. When I read this , I thought is this just another quip or does we know his numbers well?

So, here are my calculations:

9 seats at average revenue of €70 = €630

Assume four flights per day per aircraft, so 630 x 4 =€2,520.

Finally, assume 360 flying days per year, this gives 360 x €2,520 = €907,200.

Let’s not argue over the rounding, and maybe my sums and assumptions are not correct. But a round €1million per aircraft per annum adds up to a lot of money. So although O’Leary’s rule of thumb may seem like a quip, it seems to be quite a good rough measure. He is an accountant after all!

Money in Formula 1

Following from my last post, I done a little digging around and found a great article in Forbes about the money and brand valuations in the Formula 1 business. Red Bull may the new and hip brand, but Ferrari is viewed as the most valuable. Have a read here

The importance of integrating cost and risk into decision making

Olympic Stadium at Stratford, London (Photo credit: Wikipedia)

It’s always great to find and example of where some simple planning and management accounting type work would have done quite a bit for a particular company or decision.

During the summer just past, a great example came to life. The London 2012 Olympics have come and gone, but I’m sure you can imagine such an event needed a lot on planning. Mostly, the games went fine. However, a few weeks before the games kicked off, a story broke about how G4S would not be able to deliver the number of security personnel they were contracted to provide. You can read more on the BBC website here, but in a nutshell G4S racked up losses of £30-50m. Why? Well it seems to boil down to not been able to recruit enough new staff and train them within the timeframe, and thus G4S have to cover the cost of army personnel provided instead. According to the BBC, the value of the contract was £280m and one would think there should be scope for profit in this. I wonder did anyone ever ask this key question: What if we cannot recruit enough staff? If this question was asked, then the next question might be: how much will it cost us if we cannot provide enough staff. These two relatively simple questions might have forced managers at G4S to think about the risk of this happening and the costs. This does not mean they would have not faced the problems and costs they did, but at least they may have been more prepared to deal with the problem as it happened – or better still planned better from the start.

Facebook price earnings

I have written before about key financial ratios which can be used to analyse a business. Here is a great current example – the price earnings ratio for Facebook. The post is from a New York Times blog.

The effect of volume on viability – a CVP and investment example

In January 2011, a long-planned €350 million plan to build a 600,000 tonne incinerator near Dublin port finally seen work commence on the build. As you might imagine there have been many protests against the project, which would be privately operated. At the same time, the four Dublin local authorities were also planning a land-fill site north of the city. However, in January 2012, the Irish Times reported that the land-fill site plan has been scrapped. It seems that the volume of waste now being generated in Dublin does not merit a new land-fill site. And, indeed the need for the incinerator too is being questioned. It seems that due to a combination of increased recycling and lower economic activity that the volume of waste has decreased dramatically. As a management accountant, I think of this from two angles. First, from a capital investment view, someone had to decided the ultimate size of an incinerator. This would be based on a combination of commercial viability and waste volume I assume. Second, from a cost-volume-profit (CVP) view, I wonder has anyone considered the effects of volume on the “profit” (i.e. viability) of the incinerator. According the to the Irish Times article, the volume of the incinerator should be halved – which I think should mean a full re-examination of the costs and investment involved. Of course, the counter argument is it is better to have spare capacity for cover for future increases in waste generated (e.g. improved economic activity, increasing population)

In January 2011, a long-planned €350 million plan to build a 600,000 tonne incinerator near Dublin port finally seen work commence on the build. As you might imagine there have been many protests against the project, which would be privately operated. At the same time, the four Dublin local authorities were also planning a land-fill site north of the city. However, in January 2012, the Irish Times reported that the land-fill site plan has been scrapped. It seems that the volume of waste now being generated in Dublin does not merit a new land-fill site. And, indeed the need for the incinerator too is being questioned. It seems that due to a combination of increased recycling and lower economic activity that the volume of waste has decreased dramatically. As a management accountant, I think of this from two angles. First, from a capital investment view, someone had to decided the ultimate size of an incinerator. This would be based on a combination of commercial viability and waste volume I assume. Second, from a cost-volume-profit (CVP) view, I wonder has anyone considered the effects of volume on the “profit” (i.e. viability) of the incinerator. According the to the Irish Times article, the volume of the incinerator should be halved – which I think should mean a full re-examination of the costs and investment involved. Of course, the counter argument is it is better to have spare capacity for cover for future increases in waste generated (e.g. improved economic activity, increasing population)

Football and banker’s pay – there is a link?

Okay, so I have no much interest in football, but this recent piece in The Economist makes for great reading if you’re into the footie – or like me trying to paint peformance management issues in a lighter way! You can read the articles for yourself, but the basic theme is that while both banks and football clubs pay high salaries to retain/attract the best talent, the question is does this make economic sense. Arguably, the more successful banks and football clubs get to keep more of their revenues as they make more money by having the best traders/players. So it seems to make sense that pay and performance are linked in banks and football clubs. However, if bankers/players pay is capped, they can move elsewhere, which may have an effect on the performance of the bank/club they leave. So, according to the article, unless a cartel scenario exists in banks it is unlikely that any cap on pay will be useful in an economic sense. It may be what politicians want, but it’s unlikely to make economic sense.

Okay, so I have no much interest in football, but this recent piece in The Economist makes for great reading if you’re into the footie – or like me trying to paint peformance management issues in a lighter way! You can read the articles for yourself, but the basic theme is that while both banks and football clubs pay high salaries to retain/attract the best talent, the question is does this make economic sense. Arguably, the more successful banks and football clubs get to keep more of their revenues as they make more money by having the best traders/players. So it seems to make sense that pay and performance are linked in banks and football clubs. However, if bankers/players pay is capped, they can move elsewhere, which may have an effect on the performance of the bank/club they leave. So, according to the article, unless a cartel scenario exists in banks it is unlikely that any cap on pay will be useful in an economic sense. It may be what politicians want, but it’s unlikely to make economic sense.