Goodwill defined

Here is a great post from The Accounting Cafe which defines goodwill in a really nice way. Goodwill is a relatively common intangible asset, which accounting students often find difficult to grasp initially, so thanks for the great explanation.

Income, accounting and Revolut

It’s been a while since my last post, apologies. This posts recounts a recent experience I had with the digital bank Revolut, and is a good example of the need to know some basic accounting concepts.

Let’s start with a definition of income from the IASB’s conceptual framework – “income is increases in economic benefits during the accounting period in the form of inflows or enhancements of assets or decreases of liabilities that result in increases in equity, other than those relating to contributions from equity participants”. For the purposes of this post, assume I am the accounting entity.

I should say I am a fan of the digital bank Revolut (although it’s not my main bank). They are among the fintechs changing banking. At the same time, I’m cautious – I am an accountant, and from the below, you’ll see I will remain cautious

Without getting into too much personal detail, I get paid in GBP but live in Ireland so spend in EUR. I recently got a message from Revolut asking me to verify my income of €116,000. I think that cannot be right, I don’t earn that much net of taxes – I might like too :). They provided no breakdown of this amount or any ability to easily analyse it. I downloaded my statements from Revolut into Excel and did my own sums. While I could not get their exact figure, I could get close. The explanation was that transfers from my GBP to EUR account (within Revolut) were counted as income when I transfered to EUR. This is double counting, as both cannot be income. If I relate to the definition of income above, when I get paid in GBP, I get an increase in my economic benefits ( I have more cash). When I transfer this same money from GBP to EUR, it is the same money, there is no increase in the economic benefits I have – unless due to currency fluctuations, but let’s keep it simple.

Quite a fundamental and basic error occurred in the above scenario. It is yet another example of how basic accounting concepts need to be clearly understood and applied.

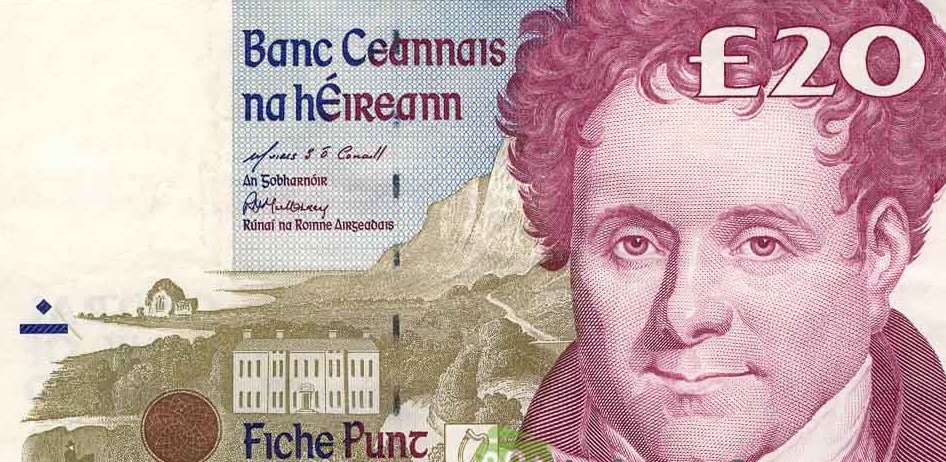

Provisions – an interesting example from a central bank

If you live in Ireland and are of a certain age, you’ll remember the above £20 note, and maybe even the older one with W.B Yeats on it. Now, we have euro notes of course, since 2002. So what if you had old pound notes? Well, when currencies change, there is usually a period of time during which the note can be redeemed at the Central Bank of the country in question. That is exactly the case in Ireland.

So where is the accounting in this you may be thinking? Bank notes have their origin in a “promise to pay the bearer on demand” as it used to say on old Irish currency, and still does on some bank notes. In other words, there is a liability on behalf of a bank to pay something – historically something like “pounds of silver”. In the case of the Irish Central Bank, there is still a liability to repay the the bearers of old currency, namely the Irish pounds. As recently reported, the Irish Central Bank has a provision in its accounts (specifically in the Statement of Financial Position) of €350 million for old notes and coins to be redeemed. This is 18 years after the notes ceased to be in circulation and be legal tender. This is why the term “provision” applies, as according to International Financial Reporting Standards a provision is “a liability of uncertain timing or amount”. In this case of the outstanding old Irish currency, the amount is certain, but the timing is not. I would imagine at some stage, the provision will be reversed, maybe 30 years for example, but until then, it will remain on the books of the Irish Central Bank.

An example of the going concern principle

One of the fundamental accounting concepts is that of going concern. In simple terms, this typically means a business is unlikely to be able to continue in operation for the next 12 months.

It is not very often the examples come to light, but recently in Ireland we had one. The national football association, the Football Association of Ireland, has their auditors state the organisation could not be deemed a going concern. According to the RTÉ news website, the auditors noted:

“While the company has received some advanced funding from UEFA during 2019 to enable the company to meet some of its current liabilities there is not sufficient audit evidence that the company will be able to meet its liabilities as they fall due. Therefore we are unable to obtain sufficient audit evidence to support the assumption that the company will continue as a going concern.”

The piece also notes the levels of debt and losses over several years. The statement above provides a nice clear understanding of what going concern means. Do have a read of the RTÉ article and other coverage to get more insights on the association.

What is a provision for bad/doubtful debts?

Photo by rawpixel.com on Pexels.com

Back to some basics today, seen as it is almost the beginning of a new academic year for me. I’d like to provide a brief summary of the notion of a provision for bad debts – based on my experience as an accountant mainly, but of course, it is something I would teach too.

First, a provision in accounting is simply an entry for something that has not yet happened but is probable. So, when a business sells on credit, it is likely some portion of customers will not pay – regardless of how good the credit controls are. Thus, based on past experience usually, the accountant in a business will create a provision for bad debts (sometimes called doubtful debts, or irrecoverable debts). At this stage, no specific debt which may be unpaid is identified, it is just a general estimate and the amount is captured as an expense in the income statement of the business. In my experience, the amount set by as a provision in the financial statements is typically about 1-3% of the amount of outstanding receivables, although this can vary from time to time. any adjustments to the amount provided are reflected through the income statement. When a debt is actually identified e.g. a customer goes bankrupt, then this specific amount is a separate expense to the income statement. Such specific debts may cause an accountant to review the amount of the provision too.

Accounting for Alcohol – part 15 “Accounting in the Port wine Chartered Trade Company (1756–1826)”

This is a brief summary of chapter 15 in our book, written by João F. Ribeiro, José M. Oliveira and Maria F. Brandão. This is also the final chapter in the book, so back to normal posts after this. I hope you enjoyed the chapter summaries.

This chapter details some accounting of the Portuguese Companhia Geral da Agricultura das Vinhas do Alto Douro (hereafter Companhia), which was founded in 1756. While also trading, the Companhia acted as a tax collector and regulation of the Douro wine sector. It was obliged to buy production excess, in accordance with the quantities determined by

the state, to avoid lowering of prices in the market. Furthermore, it acted as a creditor, as it had to lend funds to local farmers at a subsidized annual interest rate of 3%. Finally, it supervised improvement works in roads and waterways in the region, making use of collected taxes. All of this implied in needed to maintain good accounting records. The chapter provides a very detailed chart of the organisation of the accounting function and describes the various books of account maintained. The authors note how the “bookkeeping model is in harmony with the teachings of João Henrique de Sousa, the first teacher of the Aula de Comércio – the Portuguese Public School of Commerce created by Pombal in 1759”. This system was also used by other similar companies in Portugal. It is also noted by the authors that income smoothing was a typical feature after 1784, with reported earnings being very similar and accounts such as “Casks Depreciation, Bad Debt Provision, ‘Profit’ Provision and Extraordinary Income/Costs” being used to achieve this.

Accounting for Alcohol – part 2, optimism in accounting reports.

This post #2 in my summary of a recent edited book. This chapter by Alonso Moreno analyses the narrative information disclosed by a Spanish brewery, El Alcázar, from 1928–1992. The objective is to determine if the tone of the corporate reports is related to profitability. Today, the brewery belongs to the Heineken group.

The study focuses on a document entitled Memoria which is, in essence, similar to the Chairman’s Statement. Software was used to analyse the words in this report to determine the tone of the words. The tone (positive or negative) was related to other variables such as performance (profit) and the person acting Chair of the board. Over the full time period, there were more positive than negative references, irrespective of the actual performance of the company. This is a phenomenon called impression management and is something a lot of companies engage in still today. The interesting thing about this study is that overall, a positive tone dominates, despite many political events during the timeframe.

A quick lesson on blockchain for accountants: Part 2 – mining cryptocurrency

In Part 1 two weeks ago, I wrote about currency. Here, I’ll explain how “miners” help a cryptocurrency like bitcoin be useable.

In Part 1 two weeks ago, I wrote about currency. Here, I’ll explain how “miners” help a cryptocurrency like bitcoin be useable.

To be honest, I had no idea until recently what bitcoin mining actually means – and remember bitcoin is just one cryptocurrency, but I will use it here as an example.

Some weeks ago, I visited a friend of mine who owns and runs a technology maintenance firm. His office is always full of various parts of computers, but on this visit I noticed the office was quite warm and there was a hum of computer fans. So, I stuck my head around a corner and I seen something like what is in the picture above. So, joking I said, “what are you at now, mining bitcoin?”. “Yep” was the reply. So I took the opportunity to lean on my friend for some explanations.

The bottom line for me as an accountant, is that a “bit-coin mining rig” like that in the photo costs about €3,000 and can earn about €500 per month before energy costs – I will come back to these costs in a later post. So what the hell is it and what does it do I hear you ask? In my previous post, I established that bitcoin is not really a currency (yet) in the sense of dollars, euro or pounds. It also does not have a central bank behind it, or commercial banks taking it on board as a major currency. So this creates a problem, which in essence is if I want to pay you one bitcoin, how is this to be done – and remember bitcoin is an electronic medium, there are no paper notes.

Well, if I were to pay for a coffee with my credit/debit card, there is an extensive payments processing system behind the payment – think of the credit card machine, Visa/Mastercard/Amex systems and ultimately the retailer’s bank. Also, you may know that for every card transaction, the retailer is charged by the bank so they never get the full value of a card sale. For a bitcoin payment, where is the system? This is where the “miners” come in. A miner is someone who essentially processes bitcoin payments. My friend mentioned above told me the steps roughly are as follows:

- you get a rig (like the picture above). The faster the better, so rigs tend to use the fastest available memory cards – think about the graphics in a gaming console – these use really fast memory.

- Join a mining community

- Start solving hashes (encryption puzzles)- that is, process and verify bitcoin transactions. This includes working with blockchain, which will be explained in an upcoming post.

- Get a commission for each transaction

- Transfer the commission to a bitcoin wallet – for example, the Coinbase app

- Transfer to your bank account as you see fit.

So, in essence, a bitcoin miner like my friend is taking the place of the commercial banks and/or credit companies and processing payments. It is basically a form of distributed computing.

So from an accounting perspective what does this mean? Well, not very much actually. But, and this is a big but, would/could we trust people like my friend to effectively become a banking system. Personally, I am not sure. We have decades of regulation around our banking systems, and even with all the oversight, it still fails from time to time. The counter-argument could be something like the redundancy of systems or devolvement of the now rather central power of the banking and finance systems. But I’m not so sure just yet.

My next post will explain the basics of encryption.

Blockchain for accountants/accounting

I hope to write a few posts on this topic in the coming weeks, as we hear so much about blockchain and bitcoin and how it affects accounting/accountants. Before I do, this article in a great primer. For example, it relays the fact that bitcoin (for now) is an asset not a currency in accounting terms. Have a read, more to come soon.

Private companies – what accounting information is available to the public?

As you may know, there are public and private companies. Public companies can sell shares to members of the public, normally through a broker or exchange, private companies cannot. Both must prepare accounts though, and must also file certain accounting information which in turn becomes available to the public. So what accounting data can Joe Blogs get? The answer is it depends, but I will give you a good idea on this post.

In most European countries there is a central register of all companies – as far as I am aware the US does not have such a register, and the SEC focuses on public companies only. In Ireland and the UK, a small fee via an online portal gets me at least a balance sheet of a company – an abridged version for small companies – and an annual return which shows the directors and shareholders and their details (such as address). To give another example, in Germany I can download a free app called the Bundesanzeiger and search for details of any company – again for smaller companies I can get a summarised balance sheet.

For larger companies, including public a lot more information is available of course. But even with a balance sheet, or more of the company is medium or large, I can obtain quite a good picture of the financial position of a private company, and quite detailed information of directors and shareholders. Such information can be very useful to prospective investors, suppliers, customers and even employees. Why not search for a private company you know and see what you can find.

Who uses IFRS?

When I teach accounting to students with no prior accounting knowledge, I usually cover some of the regulatory framework around financial reporting. One commonly adopted set of regulations are the International Financial Reporting Standards, or IFRS.

One question often posed to me in class is what countries use IFRS? The quickest answer is lots of countries, and I often mention the big economies that don’t require the use of IFRS for public companies- the US, India and China. Recently then IFRS organisation has created an interactive map showing which countries use IFRS. The link is here, and its a very useful resource.

Fake news on accounting?

So, I was looking through Google News search to find something to quickly write for this post.

I found this article about the differences between IFRS and GAAP. I don't know much about the website, but the article has two incorrect statements. First IFRS does classify assets as current and non-current. Second, the term GAAP is more widely used that just referring to US rules. So, we could say UK GAAP or German GAAP.

Okay, so it's not fake news, but it's incorrect 🙂

The accountant as an artist?

Here is a nice post on the above from a colleague, Michael Farrell. Yes, accountants are artists 🙂

The better accountants????

This blog post appeared in my LinkedIn recently. Have a read. It’s basically claiming that British accountants are worse than their American counterparts because they don’t use technology as much as. Now, I’m a big fan of technology, but I’m also old enough to have worked before the internet and all other things which make our life easier (supposedly). The author of the blog should know that all technology is a series of instructions in some or other code, and that code is only as good as the person writing it! We are becoming way too reliant on technology and it’s no harm to do it the old way, or use less technology from time to time. If I were recruiting an accountant tomorrow, while their grasp of technology would be something I’d look out for, it’s not the only thing.

And to end, Irish accountants are best 😀

My favourite sport and accounting!

Probably my favourite (spectator) sport is motor cycle road-racing. There aren’t too many places it still happens – doing 180mph on public roads is not for everyone – but thankfully it still happens here in Ireland, the Isle of Man (IOM) and a few other places.

Probably my favourite (spectator) sport is motor cycle road-racing. There aren’t too many places it still happens – doing 180mph on public roads is not for everyone – but thankfully it still happens here in Ireland, the Isle of Man (IOM) and a few other places.

The IOM TT is probably the pinnacle of road-racing – it’s two weeks of fund each June. imagine my delight when I read an article featuring news on the 2016 TT and creative accounting! The article notes the number of TT visitors for 2016 to be similar to 2015 – based on data from the IOM government. The article also suggested a revenue of £738 per visitor for the economy, based on this same data. In the comments beneath the article, the fun starts.

One comment notes:

“This year’s TT races in June brought a £4.1 million benefit to the island’s exchequer, according to government figures just released.” OK, so that is the claimed revenue, now let’s see the total costs. And by total, I mean the total cost to the island not just the cost of TT preparations. How much for a fatality or serious injury involving medevac? How much for the road closures and effects on businesses as well as the public? These are real costs and the list goes on.

Another states:

I note the total expenditure of £738 pp is not broken down into for example travel costs and monies spent on island. Therefore that figure is meaningless If the figures of £31.3M, £22.5M and £4.1M are based on the £738pp they are also meaningless. Creative accounting it is for sure. In addition, if the government can come up with a figure for the benefit to the island they must be in possession of all costs, such as DOI, medical, policing, helicopters etc. So why do they never produce such figures?

These two sharp commentators highlight many things -the subjective major of accounting, where costs and revenues are attributed, and what are the relevant costs, for example. I’ll be using this example in my teaching at some future point.