Increasing fuel costs – Repsol provide interesting approch

With recent events in Ukraine, the world has faced a sharp rise in fuel prices. This applies to individuals and business. Here in Ireland where I live, our government has reduced the taxes on fuels, which in turn reduce the at pump price.

Repsol, a Spanish company has taken an interesting initiative. They have reduced prices of fuel by 10c per litre, but only if you pay using their app Waylet. Thinking as a management accountant, I am thinking this is quite smart on their part. I am guessing, but I would assume that paying via the Waylet app reduces many costs – such as payment processing fees, or cash handling fees for example. Thinking as a manager with a more strategic hat on, maybe Repsol are attempting to make all payments cashless, and this is a way to move more people towards their Waylet platform. Regardless, I would be confident the reduction of 10c in price is compensated by an equal cost saving somewhere.

Lean processes – the Irish Covid-19 vaccination system

Lean if a termed usually used to describe process efficiency. There are various terms used in the field of “lean” such as lean thinking, lean manufacturing/production, lean management etc, but to me the easiest way to think of “lean” concepts is to think of the normal meaning of lean – fit, strong and without fat. In organisational terms we can think of lean as being about not only doing things in a lean way, but always looking for ways to improve (or kanban).

In my time as a management accountant I have been lucky enough to be involved in projects with a lean emphasis, mainly around lean production and the notion of a pull system – where orders are pulled through the production process to meet customer delivery dates.

It has been a while since my lean experience days, and yesterday I was vividly reminded of them through a LinkedIn connection. John O’Shanahan from LeanBPI wrote a wonderful blog post of his experience being vaccinated against Covid19 in one of Ireland’s large vaccine centres. You can read the post at the link in full, but some points made by John are classic examples of lean in action. One point was how those attending had their appointment time confirmed before being allowed to enter. If someone were permitted to enter earlier or late, this could upset the process which is designed to ensure full flow through the vaccination centre. A second point relates to a Covid history check. John noted:

At the Covid-19 history check, the checker was ready to record if there was an issue but was not recording the results for all persons checked. Most patients presenting for vaccine will pass the Covid-19 history check, it makes sense to only record the exceptions and turn these patients away before entering.

Finally, the use of technology to capture information is noted. Tablets used were prepopulated with certain information from the vaccine registration portal, and little new data was captured. However, what was captured simply adds to the exist data and does not create a new process or data. I have seen other comments noting that the only paper in the process was the small card given to each person at the end (like a Vaccine ID) and information leaflets distributed. This contrasts with eight pages of forms in German vaccine centres, for example.

Do read the full post by John if you have time.

Fixed costs subsidy – a simple way governments can help business during Covid

Many governments are helping/have helped businesses during the last year since Covid 19 appeared on the scene. There are probably as many ways to help those businesses affected as there are countries in the world, and some sectors need more help than others. I would imagine from both the perspective of a business needing help, and from a government perspective, keeping this simple is key

Focusing solely on helping business with costs, probably the easiest thing a government can do is help a business with fixed costs. These costs are incurred even if a business is closed. Some such costs are imposed by government (e.g. business rates) and these are being postponed in many countries. Other fixed costs such as rent, security or insurance may still be incurred by a business, and some governments are helping business by covering a portion of such costs. Another method I have read about is how some governments are giving loans to cover such costs – as ultimately a surviving business can pay taxes, and of course government borrowing is very cheap at the moment.

Any schemes which help business by covering fixed costs should be relatively easy to operate and understand for two reasons. First, any business should have cost data to hand from its annual accounts at least, or from its accounting systems at best. Second, fixed costs are understood by even the smallest business. Of course, fixed costs are different for different businesses and sectors, and ideally any subsidy or help should take this in account.

Do you speak accounting?

It is often said accounting is the language of business. I have been recently putting this to a small test, to see how accounting works across different (spoken) languages and countries. My rather unsophisticated test stems from an experience in 2016 in Italy. While in the Abruzzo region, I came across a church in a mountain village. On it’s notice board were the parish accounts. I do not speak Italian, but my knowledge of the general format and layout of financial statements. combined some common sense, allowed me to understand the accounts quite well.

For my “test”, which I am using for a class I teach as a way to summarise various financial statement formats, I have collected the financial statements of several types/size of company and in several languages – English, Spanish, German and Irish. While I do speak some German and Spanish, my Irish is terrible (sad as an Irish person perhaps). Looking across the various financial statements in these languages – even though different rule and laws may apply – there is a typical structure which implies even a non-speaker can understand the basics. This of course stems from the fact that the double entry system underlies the financial statements, regardless of which language is used in their construction. The look and layout of the financial statements is also a good visual clue as to which statement it is – the balance sheet for example is easy to locate, given its two totals being equal.

In summary, while I am a bit embarrassed to say my Irish is terrible, I was able to understand a balance sheet in Irish – and of course in Spanish and German too. Thus, the results of my “test” – I speak accounting better than Irish!

A “living profit”? Some hints from Guinness.

Photo by Engin Akyurt on Pexels.com

A pint of the black stuff (Guinness) would be most enjoyable now, ten weeks into “lockdown”. Of course, this is not a lament to me wanting a pint, but there is link to Guinness.

For quite a few years now, media and commentators have highlighted the large profits and low taxes of many companies. Take amazon.com Inc, whose Q1 sales in 2020 reached $75 billion (see here for more), or think of Apple, Facebook or many other companies. Before I say anything further, I am not a total socialist, nor am I a total capitalist – there is a happy medium in there somewhere. You may know from reading previous posts that I do some historic research on the Guinness company. Dennison and MacDonagh (1998) in their book Guinness 1886-1939: from Incorporation to the Second World War provide some very useful insights into the general management of the company, and I will draw on one of these now.

Sometimes I ask myself why do some companies need to make so much profit? On the other hand, in a democratic/capitalist society, they are free to do so. Now, with a serious pandemic gripping the entire world, some of our underlying models are at least being questioned. So my question is could companies be happy with a “living profit”. I first noticed the term in relation to Guinness dealings with Irish malt suppliers around the turn of the 20th century. The company wished to encourage the production of Irish malt, but were not willing to buy at the lowest market price. Instead the company noted a “living profit” should be attainable. What exactly this means is not specified, but the general principle if clear. Today, most (not all) companies seem to want lowest cost everything and highest profits – presumably to keep shareholders/investors at bay. Would it not be a great improvement for us all if more and more firms took the approach of the “living profit” espoused by Guinness over a century ago? I am sure economists and others could give me many reasons why not. But, perhaps it is worth having the conversation as the business world comes back a new normal in the coming months.

Covering costs and ticking over during the pandemic – a nice example

I hope a local distillery near my home does not mind me using their graphic above. As we are all dealing with the effects of the Covid 19 pandemic, I was really impressed to see how small local distilleries in Ireland (and indeed elsewhere and some large ones too) have changed to producing alcohol based hand sanitiser.

Many businesses cannot adapt their products to the current scenario, but the example of distilleries is a really good one. The Listoke Distillery is manufacturing and selling hand sanitiser at cost. Not only is this a good thing for society, it also in my view makes business sense. As the header of this post suggests, it is better to be “ticking over” and covering costs than losing money and not covering fixed costs. I would also bet that many of us (and certainly yours truly) will remember these local small businesses that helped us out in these strange times and, hopefully, they will see increased revenues and growth. Meanwhile, with costs covered, at least they have a good chance of surviving.

By the way, I’ve just bought my second bottle of sanitiser – accompanied by a bottle of gin of course.

Book value versus market value

Photo by Chad Russell on Pexels.com

A Guardian headline in recent days says “Tesla shares soar 40% after analyst says firm’s value could hit $1.3tn“. Similar headlines could be seen in other newspapers. So, the market values Tesla at $1.3 trillion, yet their 2018 10K shows assets valued at around $30 billion, and accumulated losses of $5.3 billion. So, why are these values so different? This is something students of mine often ask. I’ll try to give a simple answer.

The market value is based on expectations for the future, and these drive up the share price – some media sources though suggest the price is being driven by short sellers trying to buy shares to cover losses they may be making as they bet against Tesla shares rising in price. Accounting values are in general based on historic cost – what was paid for something in the past. Also, for example, accounting does not include items which do not have a historic cost – such as the Tesla brand name. Thus, accounting statements do not reflect future plans or values in general. If another business were to buy Tesla, then its actual (market) values would be captured by accounting of course – brand value, goodwill and such things not captured previously. At this purchase point, there is a historic cost.

Taiwanese whisk(e)y

Yes, there are some whiskies produced in Taiwan, and they are winning some awards and grabbing attention in the whisky world. I wrote an article on The Conversation recently which looks at how Taiwanese whisky producers have some costs and cashflow advantages over other producers. You can read it here. Sláinte

Photo by Prem Pal Singh on Pexels.com

.

Private companies – what accounting information is available to the public?

As you may know, there are public and private companies. Public companies can sell shares to members of the public, normally through a broker or exchange, private companies cannot. Both must prepare accounts though, and must also file certain accounting information which in turn becomes available to the public. So what accounting data can Joe Blogs get? The answer is it depends, but I will give you a good idea on this post.

In most European countries there is a central register of all companies – as far as I am aware the US does not have such a register, and the SEC focuses on public companies only. In Ireland and the UK, a small fee via an online portal gets me at least a balance sheet of a company – an abridged version for small companies – and an annual return which shows the directors and shareholders and their details (such as address). To give another example, in Germany I can download a free app called the Bundesanzeiger and search for details of any company – again for smaller companies I can get a summarised balance sheet.

For larger companies, including public a lot more information is available of course. But even with a balance sheet, or more of the company is medium or large, I can obtain quite a good picture of the financial position of a private company, and quite detailed information of directors and shareholders. Such information can be very useful to prospective investors, suppliers, customers and even employees. Why not search for a private company you know and see what you can find.

The Tesla disconnect for me!

Ok, so I guess I will start with a caveat – I am not a fan of Elon Musk. He may be a great guy, I have never met him, but as an accountant, I see him as one of those entrepreneurs who may have good business ideas and models but they fail to turn them into profit. Tesla is a good example, and of course, I may eat my words in the future, but the company has yet to make any profitable product in a consistent manner – and they are on the third model of their car!

Ok, so I guess I will start with a caveat – I am not a fan of Elon Musk. He may be a great guy, I have never met him, but as an accountant, I see him as one of those entrepreneurs who may have good business ideas and models but they fail to turn them into profit. Tesla is a good example, and of course, I may eat my words in the future, but the company has yet to make any profitable product in a consistent manner – and they are on the third model of their car!

Looking at the Tesla 10K (which includes the financial statements) at the end of 2017, the accumulated losses are just under $5 billion. Okay, if we look at the balance sheet, the assets exceed liabilities, but some of the assets probably could lose value, or be over-valued, which would wipe any net assets. And okay, I get it that Tesla is breaking a mould, but they are not the only ones trying to make better cars. But, the company is 15 years old this year and still has accumulated losses; and the media reports production problems with the latest model still. And, it’s most recent quarter losses are about $700 million. So, let me ask this, would you invest in a company that cannot make a profit after 15 years? As an accountant, my verdict is no way!

Accounting numbers and Irish Water

I have written before about Irish Water, and the role of accounting in the on-going debate on domestic water charges in Ireland. Here is link to a recent blog post by a good colleague, Desmond Gibney at National College of Ireland.

Food supply chain and accounting

In my daily work as an accounting academic, income across many papers and articles which explore the broader role of accounting in society and out daily lives. Lisa Jack from the University of Portsmouth writes about the role of accounting in the food supply chain. This is a very interesting area, as information on costs and margins is crucial in the food sector. She has just published an article on the recent contamination of eggs in some

European countries – you can read it here. It gives a good overview of how accounting is entwined in this and other food issues, and how it could help.

Analysing a balance sheet – an insolvency example

As you may know, we can use ratio analysis of financial statements to form a view of how a business is doing. One area worth looking at is liquidity and solvency, which we can for example assess using the current ratio or other working capital ratios.

I came across a great example of a “technically” insolvent organisation recently – none less than the professional body I am a member of, CIMA. Below is an extract from their financial statements of 2016 , but first let me briefly explain what insolvency means. Solvency means a business can pay its debts as they fall due, and technically, if current liabilities exceed current assets, a business is insolvent.

If we take a look at the current assets, the total value of current assets is £18,760,000, whereas current liabilities equals £22,564,000. Thus, technically CIMA is insolvent. What makes this example even more interesting is that if we look at the current liabilities, about £13m is deferred income, the subs in advance. These are already included within the cash balance, or the cash has been spent already, so they are not really a liability per se. However, if CIMA were to close tomorrow, it would have to repay these subs to members. So the cash in the bank more or less could cover this, but then if all receivables were paid they would not cover the payables.

Have a look at the full accounts at the link above if you want to see more.

Storytelling and numbers

Everyone loves a good story. But should accountants tell stories? Here is great post I found in LinkedIn which shows the value of stories

Everyone loves a good story. But should accountants tell stories? Here is great post I found in LinkedIn which shows the value of stories

Some insights from IAG

IAG, or the International Airlines Group, is the the parent of Aer Lingus, British Airways and Iberia. In my university, we were lucky enough to have their CEO, Willie Walsh, speak to us before Christmas.

IAG, or the International Airlines Group, is the the parent of Aer Lingus, British Airways and Iberia. In my university, we were lucky enough to have their CEO, Willie Walsh, speak to us before Christmas.

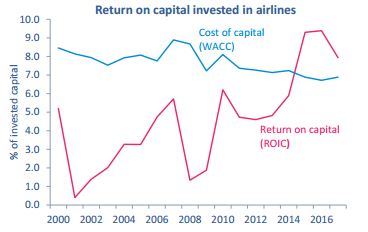

Some things he mentioned are relevant to this blog, and of course interesting. One thing Mr Walsh noted was how only in recent years has the airline sector actually made a return on capital. This must be attributable in some way to a focus on cost by the sector in recent years. The chart below from IATA shows what I mean. As you can see, the cost of capital was higher than the return until 2014.

As my last post indicated, a focus on cost and efficiency has been a feature of the airline sector in recent years. To give another example, Mr Walsh cited an example of using two larger aircraft on a route without a loss in passenger capacity. So fuel, crew and capital cost all decrease in such a scenario. In addition, it freed up a slot at London’s Heathrow airport, which can then be used to generate more revenues.