Food supply chain and accounting

In my daily work as an accounting academic, income across many papers and articles which explore the broader role of accounting in society and out daily lives. Lisa Jack from the University of Portsmouth writes about the role of accounting in the food supply chain. This is a very interesting area, as information on costs and margins is crucial in the food sector. She has just published an article on the recent contamination of eggs in some

European countries – you can read it here. It gives a good overview of how accounting is entwined in this and other food issues, and how it could help.

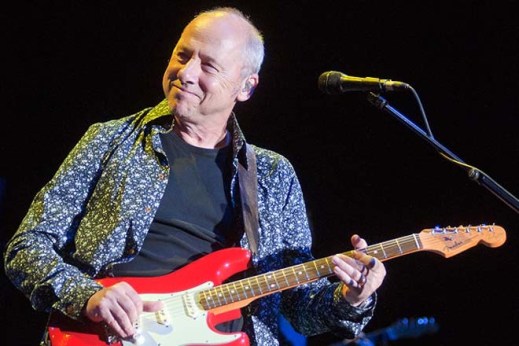

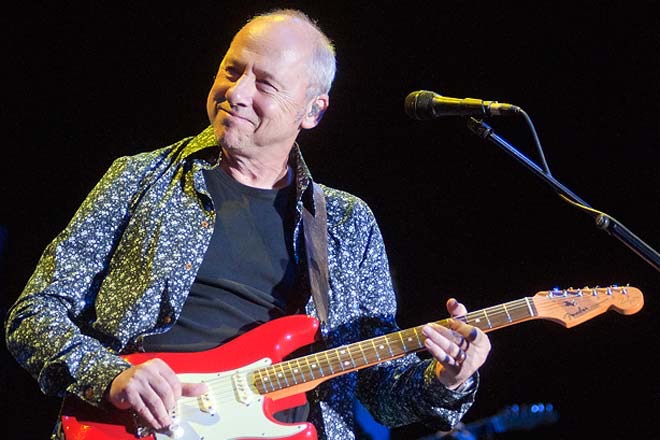

Marginal costs and revenues – at a Mark Knopfler gig

Twenty five years ago, I first saw Dire Straits live in Dublin. It was one of the first gigs I ever went to. Back then, there was a guy on O’Connell St in Dublin selling bootleg cassettes of live gigs for maybe £5. The quality was awful, but fans loved it. And it was illegal of course, making it all the more fun.

Move forward to 2015, and I was lucky enough to see Mark Knopfler live in Leipzig. Still an amazing guitarist. Of course, times have moved on and almost everyone has a smartphone to record a gig on – I hate doing this, but some artists don’t seem to mind. To my surprise, Knopfler in his 2015 tour not only seemed to encourage recordings at gigs, but found a way to make some extra revenue.

At each gig – including Leipzig, and yes, I did buy – you could download the actual gig recording for €15. This was sound desk quality, and unique. Add an extra €20 and you got the recording posted to your home on a souvenir USB stick.

Now think of this in marginal costs and revenues. The marginal cost is close to zero, as the stadium is fitted out, staff there and the sound desk set up. Maybe the only cost is a bit of rented space on a cloud server somewhere. On the revenue side, it is pretty much a no-brainer really – the full amount of the €15 per download is revenue, as I just argued the cost is close to nil. So if 1,000 fans at each gig buy the recording, that’s €15,000 x maybe 20 gigs = €300,000, a tidy sum. And of course, it is a legal recording 🙂

CVP Analysis in action – the TGV

(Image:Wikpedia)

A few weeks ago I posted a piece on costs and profits when there is too much volume in the market. This post takes a look at the TGV (high-speed) service of SNCF. It’s in a spot of bother in terms of profit and management are considering various options.

I have been on the TGV several times. It is a fabulous service, but in today’s low-cost flight era it’s a bit expensive. And that’s exactly what a recent post from the Economist noted. According to the post, many TGV routes are no profitable. The reason for non- or low profitability is two-fold 1) increased competition from low-cost airlines who entice passengers with lower fares and 2) increasing costs paid to the rail track operator. SNCF management have apparently suggested three possible solutions, as follows:

1) decrease volume – i.e. reduce routes to those which are more profitable and attract adequate passenger numbers

2) increase volume, by lowering price. This could attract passengers back from low-cost airlines. It is a risky option though, as failure to attract enough passengers could worsen things

3) overhaul operations to be more like a low-cost airline i.e. become more cost conscious and efficient.

Which ever of the above three options are chosen, it is a classic case of the application of Cost-Volume-Profit (CVP) analysis. The costs and revenues will determine how profitable the TGV routes are, but so will the volume available. For example, using option 1 may improve profitability, but may not address costs or revenues. It may also be a bad option politically. Option 3 might keep service volume, but increase profitability and maintain pricing. And, as mentioned, option 2 might increase profitability if passenger volumes increased. It is not to hard to imagine a management accountant at SNCF using CVP techniques to show managers possible outcomes of each option.

Break even in farming

Farmer’s, even if they know their costs, face a problem in that they can’t do anything about crop prices. If the price is above break even, it may even make sense to rent more land to grow more.

And of course, if a farmer knows the break even ‘cost’ per acre/hectare then they can try to get the best price above that.

Here is a good article showing the costs of corn this year, and working out a break even price. It’s a good example of the application of break even analysis.

Promotions on price

As a management accountant, when price is dropped we probably want to be sure that we still make a profit- or at least cover cost. An article I found on inc.com gives some very useful hints to ensure that price promotion is effective in the longer term. Your can read is at this link.

US Postal Service – reduced volumes = reduced costs

(Photo credit: Wikipedia)

In February this year, the United States Postal Service (USPS) decided to cease delivering mail on Saturdays. While this may be seen as inconvenient for some personal and business users, in management accounting terms it is probably a simple cost-volume issue.

Mail volumes have fallen globally due to email and other communications media. With falling volumes, a postal service would either have to reduce costs or increase revenues to maintain profits – or keep state subsidies low. Increasing revenues may be difficult given the competition is sectors such as parcel deliveries, which have increased in volumes. It is also difficult to raise postage rates given the political and/or state involvement. So this leave costs, or more specifically cost-cuts, to get things back in balance. Apparently, ceasing Saturday deliveries will save $2 billion annually. You can read more here from The Economist

London Underground – profitability and costs in the early days

London underground (Photo credit: @Doug88888)

I have been reading a book recently on the history of the London Underground. It’s called Underground to Anywhere by Stephen Halliday and I actually bought it in the London Transport museum, on Covent Garden. Of course the tube is 150 years old this year, and you will find more about that here.

Reading the book I was quite surprised by how much accounting was in there. Two things stand out from the early days of the tube which related to accounting. First, the financing seemed to be quite precarious. As each line was built by private companies, private finance was raised. And when results proved less than expected, it seems quite a bit of creative re-financing went on. The author actually notes that without the somewhat suspect and complex financing, London’s Underground may not have grown to what it is today.

The second thing was the fares structure in the early days. Before lines were connected, the fares seemed to have been standard at say 2 pence. However, the author notes that the various companies started to raise and lower fares and certain times, or lower fares overall to increase passengers numbers and revenue- a classic cost, volume profit (CVP) scenario.

Kindle Fire breaks even – but profits elsewhere

Image via CrunchBase

I have written a few posts before on breakeven, but here is a great example of how businesses are prepared to accept not making money on some products, for the sake of others. In October 2012, Amazon launched its Kindle Fire tablet and its Paperwhite e-reader in the UK and other European countries. The Kindle Fire retails at about £150, which is probably less than half the price of an iPad and about £100 cheaper than an iPad mini. In an interview with the BBC , Amazon’s boss Jeff Bezos said the company sells its hardware at cost i.e. they breakeven. This may explain the cheaper price of the Kindle Fire compared to the iPad. However Amazon earn profits on Kindle book sales, Kindle book rentals and its Prime service. In contrast, Apple have noted they breakeven on services such as iTunes and make profits on their hardware,

An innovative approach to pricing – life cover at a fixed price

(Photo credit: aWee)

Any business needs to understand its costs to be able to set a price – at least that’s one of the key things I would tell my students when I teach management accounting. Of course, another key point to mention is that sometimes the price will be dictated by the market the business is in.

If you read any of my posts, you know I like to give examples of topics I am interested in or teach. The Irish economy is not doing the best still, so I think it would be fair to say that consumers are price conscious and looking for a good deal. This means the market is leading the price to an extent. So what can you do as a business in this case. One thing is to try to reduce costs so that you make a profit at the market price. Another option is to change the product/service you offer – and I cam across a great example of this recently.

A new website emerged called www.10eurolifecover.ie. Normally, if you want to buy life assurance, you go to a broker/website and give the amount of cover you want – say €100,000. Based on things like your age and health, you get a price for the amount of life assurance cover requested. What this website does is fixes the price at €10 per month, and then tells you how much cover you can get for that amount. The idea seems like a great way to price in a market where consumers are probably more concerned with what they can afford than with the amount of cover they get.

Pricing tips for small business

I’m a bit lazy today, sorry, so I’m directing you to a nice post on setting prices in small online business: Top 5 pricing tips for small business

Rising prices, holding prices – Primark holds retail prices steady

With some commodity prices on the rise, and continued economic woes, some businesses are holding retail prices and reducing margins. Associated British Foods, which includes the low price high-street retailer in Primark (UK/Ireland and some European countries) is an example. In late April 2011, the company reported it wished to absorb material price increases rather than pass them on to end-consumers. Increasing sugar and cotton prices reduce the company’s margins. However the CEO reported that the company did not want to relent it’s status as a low price retailer in the clothing sector.

With some commodity prices on the rise, and continued economic woes, some businesses are holding retail prices and reducing margins. Associated British Foods, which includes the low price high-street retailer in Primark (UK/Ireland and some European countries) is an example. In late April 2011, the company reported it wished to absorb material price increases rather than pass them on to end-consumers. Increasing sugar and cotton prices reduce the company’s margins. However the CEO reported that the company did not want to relent it’s status as a low price retailer in the clothing sector.

Setting prices in small business

Setting a price for a small business can be a challenge. Cut the price too much and you loose money. Raise the price and you loose business. An article in the New York Times recounts the experience of some US small business. The basic message is that price is not everything. One business owner recounts how the quality customers gained outstrips those lost due to a perceived high price. Here’s one story

Setting a price for a small business can be a challenge. Cut the price too much and you loose money. Raise the price and you loose business. An article in the New York Times recounts the experience of some US small business. The basic message is that price is not everything. One business owner recounts how the quality customers gained outstrips those lost due to a perceived high price. Here’s one story

“About three years ago a computer error caused all of the prices on Headsets.com to be displayed at cost rather than retail. With the lower prices on display for a weekend, Mike Faith, the chief executive, expected sales to soar. Instead, the increase was marginal. “It was a big lesson for us,” Mr. Faith said.”

The basic lesson from this experience is that customers don’t think price is the be all and end all. The experience of a gluten free flour business showed that competitors prices may not matter as much as one thinks too. The company managed to raise its price by 20% in the first year in business by convincing customers that the product had more added value than competing flour. The most important lesson mentioned is that costs must be covered in the price charged. Seem so obvious, but I have written several pieces on this blog about breaking even.

How to price your products or services

Setting a price is a very important task for any business. Set the price too high and sales may not come; set it too low and you might not make money or customers might perceive your product/service as poor quality. As an accountant, I would of course first think of costs – without a clear knowledge of what your cost base is, how can you sell something at a profit. But other things determine price too, like the customer and the competition. Given that I’m sort of on holidays, and writing accordingly, here’s a great piece from inc.com that will help you set a price.

Setting a price is a very important task for any business. Set the price too high and sales may not come; set it too low and you might not make money or customers might perceive your product/service as poor quality. As an accountant, I would of course first think of costs – without a clear knowledge of what your cost base is, how can you sell something at a profit. But other things determine price too, like the customer and the competition. Given that I’m sort of on holidays, and writing accordingly, here’s a great piece from inc.com that will help you set a price.