The end of low cost air fares?

Over the years, I have used lose cost airlines as examples in several of my blog posts. Carriers like Ryanair have always interested me – whether you love them or hate them they are successful.

A recent article on RTE’s business section gives a good summary of the low cost sector, but also considers how costs have and will increase, leaving no option but to increase fares. You can read the article here.

The Tesla disconnect for me!

Ok, so I guess I will start with a caveat – I am not a fan of Elon Musk. He may be a great guy, I have never met him, but as an accountant, I see him as one of those entrepreneurs who may have good business ideas and models but they fail to turn them into profit. Tesla is a good example, and of course, I may eat my words in the future, but the company has yet to make any profitable product in a consistent manner – and they are on the third model of their car!

Ok, so I guess I will start with a caveat – I am not a fan of Elon Musk. He may be a great guy, I have never met him, but as an accountant, I see him as one of those entrepreneurs who may have good business ideas and models but they fail to turn them into profit. Tesla is a good example, and of course, I may eat my words in the future, but the company has yet to make any profitable product in a consistent manner – and they are on the third model of their car!

Looking at the Tesla 10K (which includes the financial statements) at the end of 2017, the accumulated losses are just under $5 billion. Okay, if we look at the balance sheet, the assets exceed liabilities, but some of the assets probably could lose value, or be over-valued, which would wipe any net assets. And okay, I get it that Tesla is breaking a mould, but they are not the only ones trying to make better cars. But, the company is 15 years old this year and still has accumulated losses; and the media reports production problems with the latest model still. And, it’s most recent quarter losses are about $700 million. So, let me ask this, would you invest in a company that cannot make a profit after 15 years? As an accountant, my verdict is no way!

Unbundling costs at low cost airlines

A few weeks ago, I read a nice article in The Telegraph by David Millward on one of my favourite topics, airlines and  all things to do with airports – I was born close to Dublin Airport and it was a big part of my growing up.

all things to do with airports – I was born close to Dublin Airport and it was a big part of my growing up.

Anyway, many of us have witnessed the phenomena of low-cost airlines emerge of the last 20-30 years, and as an accountant it’s the constant actions to reduce costs that amaze me. As Millward said in his article, one of the things that airlines have done is unbundle. This means you get the basic fare from origin to destination for as low as possible. If you want more you pay more. This is fine by me, on a shorter flight, but now as longer-haul low-cost carriers appear I am not sure – I have no experience yet, so I dare not say. The low-costs have of course eaten into some of the legacy carrier market, but they have also expanded the market by making flying more accessible. Millward suggests that the low-costs have by now probably stripped out all they can to reduce costs, but the legacy carriers can do more – if they wish. I read another article recently which mentioned how WestJet, a low-cost transatlantic carrier remove the in-flight screens to save 500 kg in weight and thus save fuel. They replaced the screens with a wi-fi system and the BYOD idea – most people have their own device on-board anyway. Surely such simple steps could be taken by any carrier.

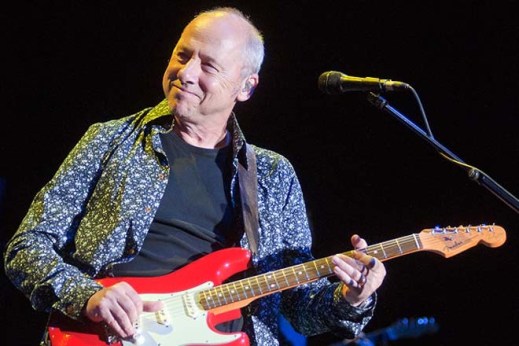

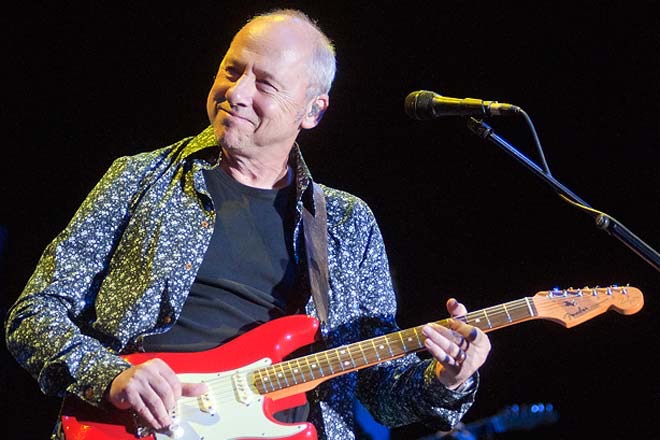

Marginal costs and revenues – at a Mark Knopfler gig

Twenty five years ago, I first saw Dire Straits live in Dublin. It was one of the first gigs I ever went to. Back then, there was a guy on O’Connell St in Dublin selling bootleg cassettes of live gigs for maybe £5. The quality was awful, but fans loved it. And it was illegal of course, making it all the more fun.

Move forward to 2015, and I was lucky enough to see Mark Knopfler live in Leipzig. Still an amazing guitarist. Of course, times have moved on and almost everyone has a smartphone to record a gig on – I hate doing this, but some artists don’t seem to mind. To my surprise, Knopfler in his 2015 tour not only seemed to encourage recordings at gigs, but found a way to make some extra revenue.

At each gig – including Leipzig, and yes, I did buy – you could download the actual gig recording for €15. This was sound desk quality, and unique. Add an extra €20 and you got the recording posted to your home on a souvenir USB stick.

Now think of this in marginal costs and revenues. The marginal cost is close to zero, as the stadium is fitted out, staff there and the sound desk set up. Maybe the only cost is a bit of rented space on a cloud server somewhere. On the revenue side, it is pretty much a no-brainer really – the full amount of the €15 per download is revenue, as I just argued the cost is close to nil. So if 1,000 fans at each gig buy the recording, that’s €15,000 x maybe 20 gigs = €300,000, a tidy sum. And of course, it is a legal recording 🙂

Apple’s numbers

As you may know, profits at Apple for Q4, 2014 were some $18billion. This is reportedly the largest quarterly profit in history.

One of the things accountants often do is use ratios to compare businesses from one year to another and with other businesses. With such a large profit at Apple, I’d begin to think that any comparisons might not be of great value. So is there any way we could our such a number is perspective. Certainly Apple could probably clear all Irish sovereign debt with there cash pile, but here is an interesting presentation from the BBC

Flat rate taxi fares, Hailo – reducing taxi costs?

I recently got a flat rate taxi fare from an airport in Europe – a bit of an adventure, the guy was really moving it. And the rate was of course cheaper than normal taxi fare which at airports are usually more expensive . So then I started to think about apps like Hailo (and the latest one Uber). Can these reduce taxi costs and in turn give us cheaper fares. Well I guess so. I don’t know for sure, but I would assume using Hailo is cheaper than “renting” a radio and a customer base from a taxi firm. If I’m right, will these reduced costs be passed on?

How the cloud makes businesses possible

I have written a few posts previously on cloud computing and how it affects costs, software and business models.

I came across a nice article in Forces which details how businesses like Instagram and Snapchat can use the cloud to grow very quickly at minimum cost. Once such businesses grow, they can acquire a large value (e.g. WhatsApp recently), without actually having much in terms of what accountants would associate with value i.e. assets.

You can read the full article here.

Operating leverage – seasonal woes at UPS & Fedex

Apparently, logistics firms UPS and Fedex ran into a bit of bother during the pre-Christmas parcel rush – see this article on Forbes by Steve Banker.

The problem may be one of bad planning. Simply put, Steve Banker suggests both firms did not have enough capacity in terms of aircraft or parcel sorting at their highly automated distribution centres. While Banker talks about strategic planning, when I read his article I immediately thought about operating leverage – which would of course be part of the strategic planning.

Operating leverage can be simply defined as the percentage of fixed costs compared to total costs. If UPS or Fedex wants to add capacity, by either leasing aircraft or adding more automation, this will increase fixed costs and operating leverage worsens as these fixed costs affect profits. Alternatively, firms like UPS or Fedex could instead hire more temporary staff, which represents a variable cost. No doubt they do this, but from my limited knowledge it would seem Amazon have this well organised. Increasing variable costs does not affect operating leverage, and is thus preferable in the longer term.

Of course it may be that firms like UPS and Fedex actually need to increase capacity and thus fixed costs. But as Banker points out in the Forbes article, investing to cover short term seasonal capacity issues implies over or idle capacity at other times.

Stick to the cooking – restauranteurs and accounting knowledge?

Cuisine 3 etoiles de Jacques Lameloise (Photo credit: Wikipedia)

In October of this year, Michelin star chef Derry Clarke had a go at Dublin restaurants selling “cheap meals” – see here. I guess Clarke was thinking from his own view when he said “the number of restaurants offering meal deals at economically non-viable prices just isn’t sustainable, it’s the same cost in McDonalds, but we have all of the overheads”.

He may have a point about the number of restaurants being sustainable, but Derry, stick to the cooking. Any management accountant could figure out that even if meals are sold cheap (and I doubt they are below cost as Clarke suggests), they still make a contribution towards overhead costs. It would be better to have 50 guests in a restaurant earning a contribution of €5 a head (€250 in total) than having an empty restaurant. In the latter case, costs such as labour, heating, rent and so on are still incurred.

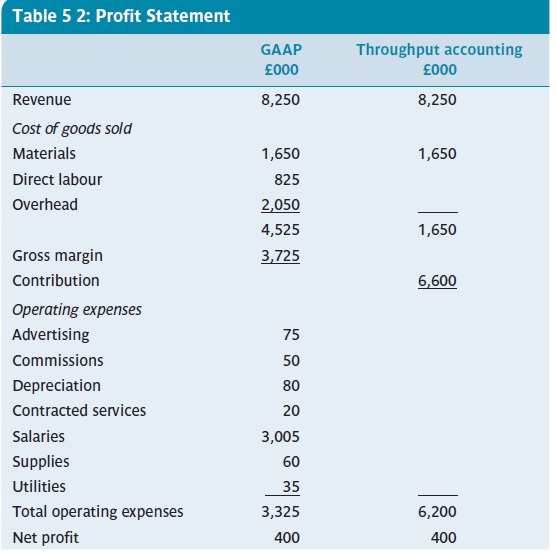

What is throughput accounting?

Throughput accounting is an alternative to traditional internal cost reporting. It stems from the Theory of Constraints, which I won’t detail here, but essentially this theory suggests an organisational can best achieve its goals (e.g. profit) by maximising it use of a constraining resource. A constraint could be machine capacity for example, and by maximising throughput on the constraint profit is maximised. To report on throughput, a new accounting approach is required, called throughput accounting:

1) Totally variable costs – this means a cost which is incurred only when a product/service is created. This often means only material costs. Labour costs are not totally variable, as employees are typically paid regardless. Some transportation or subcontracting costs may be totally variable. All overhead costs are not totally variable.

2) Throughput – this refers to revenue less totally variable costs. Contribution using throughput accounting is likely to be higher.

3) Operating expenses – this refers to all costs other than totally variable costs. Operating expenses are not distinguished into categories such as fixed or variable, or allocated to products in any way i.e they are similar to period costs, as they are costs which are more

associated with the passage of time than with products.

4) Net profit – in throughput accounting, the net profit is simply throughput minus operating expenses.

Looking at 1-4 above, you can see no attempt is made to allocate any overhead cost, so throughput accounting does not meet normal GAAP requirements. It does however raise the possibility of selling products/services at a price which is lower than under normal cost accounting, and it may also be useful for short-term decision making. Below is an example of a profit statements from Burns et al (2013. p. 112), which shows how throughput accounting produces a differing view on costing.

The overall net profit figure is exactly the same, but you can see a much bigger contribution under the throughput method. Arguably, as only material costs (in this example) are totally variable, a report such as the one above is very useful for short term decision-making.

References:

Management Accounting, Burns,Quinn, Warren & Oliveira, McGraw-Hill, 2013 – see burnsetal.com

Speed cameras business

In July this year (2013), I read an interesting brief news report about a speed van operator in Ireland. Yes, we all hate these guys, but the article made me realise this seems like a good business to be in – even if you are hated by motorists. According to the article, the GoSafe consortium makes a profit of almost €50,000 per week or €2.5m per year. It has almost €11m debt and is contracted to provide 6,000 hours per month to the Irish state. The article notes that at least one motorist per hour is caught speeding. I don’t know the ins and outs of the contract, but if the company makes a profit of €2.5m annually, even if it does pay out some dividends, the debt owing could be paid down quickly it would seem. The management accountant in me would really like to know what is the breakeven number of speeding motorists per day! You can read more at this link: http://www.rte.ie/news/2013/0720/463662-speed-vans/

Management accountant’s travelogue – part 3 – to toll or not to toll?

(Photo credit: Wikipedia)

As I drove through France and Spain on my holiday, I thought about the tolls one must pay (on most) motorways. I was thinking how do they set the prices of these tolls? Of course, public infrastructure like motorways is often now financed by a combination of public and private investment. Regardless of the investment type, can you imagine how tricky it is to pitch a price for a motorway toll. If it’s too high, less will use it (M6 Toll in the UK) and costs take much longer to be recouped. Set it too cheap and it floods with traffic, which in turn eventually results in less users, and that equals less money. Should the price be set with future investment and on-going maintenance in mind. Should it be a social good with a very low price – but then where will the money come from for re-investment? Lots of questions here, but I hope you can see a lot of management accounting is behind these decisions. I would imagine getting the initial price correct is the toughest part. Nowadays though, I am sure there are plenty of modelling tools to help toll operators and governments.

Management accountant’s travelogue- part 2 – merendero

from a pi...")

While in Northern Spain – Asturias to be exact – we were invited one evening to a meal at a merendero. From my limited knowledge of Spanish, this translates loosely to a picnic area. What we in fact had was a lovely tapas evening in a restaurant with a merendero attached. I have written before about business being child-friendly, or not as is often the case. The merendero concept is so simple; a lot of picnic tables, some play areas/equipment, a simple ordering system where you collect you food. And, all this at minimum cost to the restaurant I would imagine – at least in fixed costs. On the revenue side, the turnover of the restaurant is probably increased quite a bit as 1) more parents come and 2) future customer (the kids) are secured. In the particular merendero we visited, there were at least 100 places outside for people to eat and drink – a sizeable increase in volume without equally high costs. If only the Irish weather were good enough to do this! But, I’m sure a clever restaurant owner could take some of the idea and increase their business success (and revenues).

The best private companies do …what exactly to be successful?

Short post this week , but no less interesting I hope. Here’s a link to a nice article on Forbes which gives the key habits of successful private companies. Article

Kindle Fire breaks even – but profits elsewhere

Image via CrunchBase

I have written a few posts before on breakeven, but here is a great example of how businesses are prepared to accept not making money on some products, for the sake of others. In October 2012, Amazon launched its Kindle Fire tablet and its Paperwhite e-reader in the UK and other European countries. The Kindle Fire retails at about £150, which is probably less than half the price of an iPad and about £100 cheaper than an iPad mini. In an interview with the BBC , Amazon’s boss Jeff Bezos said the company sells its hardware at cost i.e. they breakeven. This may explain the cheaper price of the Kindle Fire compared to the iPad. However Amazon earn profits on Kindle book sales, Kindle book rentals and its Prime service. In contrast, Apple have noted they breakeven on services such as iTunes and make profits on their hardware,