Customer support costs – should “difficult” customers be charged more?

A simple answer to the question posed in the title above is yes. This is because such customers use up more time and resources and should be charged more. If you have learned activity-based costing or activity-based management in your studies of management accounting, you will also know that such techniques try to allocate costs based on the resources used. Thus, a more time-consuming customer will pay more.

Of course, it is not that simple. You may not be able to charge customers more, or your business may be a service provider with back-end or post sale support. The latter case is what inspired me to write this post. My better half works for a large financial institution. She often tells me how customers are asked several times for the same thing e.g. documentation to prove their address, their age or even their identity. Some seem to ignore requests, not provide full information or deliberately try to hide some information. Getting back to the customer a second or more times adds to cost. Thus, the management accountant in me thinks I should charge these customers more. In normal circumstances no organisation would. But what if, as a bank for example, I asked a customer three times to provide a scan of their passport for identity purposes and each time they blanked out the date of birth? This would imply much more effort (and cost) was needed than should be. If it were up to me, I would say to the customer “ok, €/$/£25 please, as you as wasting time”. I guess no banks would be gutsy enough to do something like this, but maybe it would make for greater efficiency as customers would comply more the first time. I am just using a bank as an example here, I am sure there are many other scenarios where customers could be dissuaded by threat of a greater price/charge like this.

Construction cost management at BER airport

Cost need to be managed. This is term I have probably heard or said many hundreds of times in my life as an accountant and teacher. Managing costs requires two things 1) a knowledge of costs and how costs are structured in the business, project or product and 2) managers. We probably take both of these for granted, but there are some classic examples of when one, other or both do not apply.

If you have ever been involved in a building project, or built your own house, you will know that construction costs are notoriously difficult to manage. Just think of any large building project in your country, was it delivered on time and within budget? Sometimes the answer is yes, but when it is no, it can be a resounding no. Take for example the Berlin airport which is due to be open on 31/10/2020 – probably the worst time in aviation history to open an airport due to the present pandemic. This project started back in 2006, and it is being opened at a cost which is billions in excess of plan. So what went wrong? I could probably write a book about it, but in essence bad management. Of course a large project may be late and over budget, but in the case of Berlin airport, the delay is about a decade and the cost overrun about 3 times. A BBC News article provides a good summary, and I will give some examples. First, there were changes during construction due to plans not including shops for example. This added time and money. Te question has to be how did the “managers” not notice a part of the airport which can give 50% of revenues was not there? Second, there were issues due to there being no specialist contractor, rather many smaller ones who the managers hoped could be compelled to reduce costs. However, not having a single point of contact in a the form of a specialist contractor implied the project management was very complex – and thus costly.

This is just a brief summary. Have a search around to find out more. Here is a nice article on the technical side, or here from CNN – which includes a final cost estimate of €7.3 billion (original plan c. €2 billion)

Photo by Negative Space on Pexels.com

Storytelling and numbers

Everyone loves a good story. But should accountants tell stories? Here is great post I found in LinkedIn which shows the value of stories

Everyone loves a good story. But should accountants tell stories? Here is great post I found in LinkedIn which shows the value of stories

Loss-making rail routes in Ireland

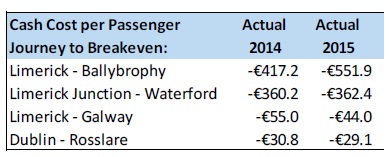

Image from irishrail.ie

A review report by the Irish National Transport Authority published in 2016 makes for some interesting reading. It highlights the issues faced by many rail companies world-wide in that not all routes are profitable. When this occurs, many States subsidise services in the general public and social interest.

The 2016 report includes an interesting use of a breakeven approach to identify poorer performing routes. The analysis calculated the cash per journey required to breakeven. This was done by taking total cash costs less revenue divided by the passenger journeys on each route. The report notes that all government subvention, capitalisation, depreciation and exceptional costs were excluded. It identified four poorly performing routes, as shown below.

What this graphic shows taking the first route as an example is that about €550 per passenger journey is needed to cover what we might classify as the running and maintenance costs.I like its simplicity, and I don’t think anyone would be prepared such a fare. Using such figures, the rail company or the State has to decide if it can subvent to that amount on an on-going basis. The latter to routes seem to be more workable in terms of a combination of increased fares, cost cuts and/or subvention.

Charities as businesses?

In recent weeks, the Irish media has revealed yet another charity mis-using funds – this time the founders used a lot of the charity monies for personal purposes.

In recent weeks, the Irish media has revealed yet another charity mis-using funds – this time the founders used a lot of the charity monies for personal purposes.

Regulation of charities in Ireland is not as good as it could be – we have some legislation waiting to be enacted since 2009 as far as I know. But laws cannot prevent what happens within an organisation from happening; they can only penalise after the event.

So what bugs me? Well, the title of this post really – it is something I picked up from the print media in recent weeks. I am sure I have said somewhere on this blog that accounting is the language of business, so what about accounting for charities? My own opinion is that charities must have proper accounting, and there are accounting standards already in place for charities. But I often wonder should we be careful and not allow charities to become too much like a business? For example, we should be using accounting in charities to drive efficiencies, not necessarily monitor revenue and costs like in a business. Nor should we be using accounting just to get funding for a charity. In short, what I am trying to say is that we need to be careful and try to not let accounting (and other commercial sector notions) detract from what a charity should be.

What is wrong with this headline “Tesco delayed payments to suppliers and boosted profits”

Image from journal.ie

So what is wrong with above statement? Simply, it is the application of the accruals concept in accounting. Under this concept, revenues and expenses are matched, and when cash is received/paid is not relevant – at least in the calculation of profit.

Here is a simple example. Let’s assume a business sells goods for $1,000 cash but has not paid the supplier. The goods cost $600. The profit on this is $400. If the supplier is never paid, or is paid in 10 days, the profit will not change.

While the article is incorrect in terms of the title, it’s message is solid – that you can benefit by not paying people. In the simple example above, the business has $1000 in the bank.

What is lean accounting?

Defining lean accounting is a bit odd to me, as I don’t really buy the idea that there is a technique called “lean accounting”. Having said that, there is definitely a concept called lean manufacturing. In a nutshell, lean manufacturing implies three concepts – pull, flow and waste reduction. Pull means product is produced (or pulled) according to customer demand. Flow means product moves through a facility as efficiently as possible and no delays. Both of these should imply waste reduction.

So what does this mean for accounting. Well one thing is inventory reduction. Another may be capital investment to get things working well. Both might put accountants off! But rather than me rattle on, here is a very nice article from Forbes which explains lean accounting and some issues.

Non-financial performance measures – example of one difficulty from Deutsche Bahn

According to a report in Der Spiegel, German rail company Deutsche Bahn has had quite an increase in the volume of customer complaints last year (2013). Complaints reached a new record in fact and were 50% higher than previous years.

For a rail company, customer complaints are probably one key non-financial performance measure. Ideally, the complaints should be as low as possible and I am sure a there’s a target in Deutsche Bahn on this measure. Reading the report though, it’s easy to see why using non-financial performance metrics can be tricky. Apparently the increase is down to ow things. First, more complaints arose due to poor weather – something beyond anyone’s control. And second, a new system for customers made it easier to complain. So, a simple year on year comparison of customer complaints would be quite useless. Maybe even setting a target is tricky too, as weather, strikes and many other non-controllable factors could come into play.

Despite such difficulties with non-financial measures, they will always augment monetary measures. While money is typically quite a stable measure , it can’t capture qualitative factors like customer satisfaction.

Building a better income statement – according to McKinsey

McKinsey have a nice web article which highlights the problems with GAAP reporting versus the needs of investors and analysts. The kernel of their article is that financial statements, with some small adjustments, could save investors a lot of re-working of figures. They provide the following example:

Image copyright McKinsey

Two things come to my mind. First, in my first real management accounting job almost 20 years ago now, we prepared an income statement which was not too far away from the one on the right above. And, most management accounting courses would teach students to draw up some kind so similar profit statement – at least separating direct and indirect costs.

Second, the articles does not mention XBRL at all. With tagged data from GAAP financial statements, XBRL could re-draw financial statements in any format. I am not saying all XBRL tags are there to do what McKinsey suggest, but it is certainly possible technically.

You can read the full article at the link below. It is worth a read.

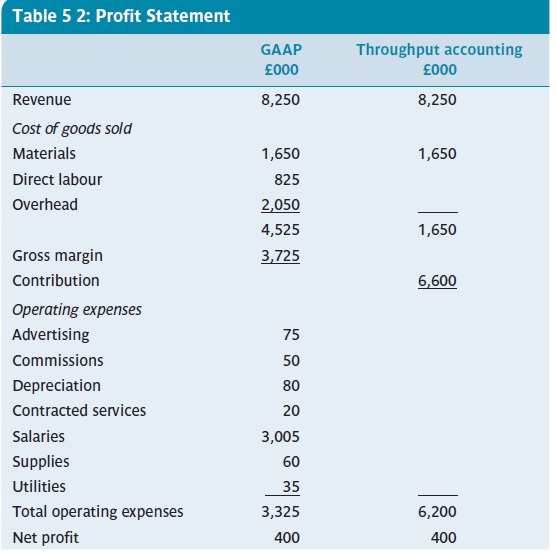

What is throughput accounting?

Throughput accounting is an alternative to traditional internal cost reporting. It stems from the Theory of Constraints, which I won’t detail here, but essentially this theory suggests an organisational can best achieve its goals (e.g. profit) by maximising it use of a constraining resource. A constraint could be machine capacity for example, and by maximising throughput on the constraint profit is maximised. To report on throughput, a new accounting approach is required, called throughput accounting:

1) Totally variable costs – this means a cost which is incurred only when a product/service is created. This often means only material costs. Labour costs are not totally variable, as employees are typically paid regardless. Some transportation or subcontracting costs may be totally variable. All overhead costs are not totally variable.

2) Throughput – this refers to revenue less totally variable costs. Contribution using throughput accounting is likely to be higher.

3) Operating expenses – this refers to all costs other than totally variable costs. Operating expenses are not distinguished into categories such as fixed or variable, or allocated to products in any way i.e they are similar to period costs, as they are costs which are more

associated with the passage of time than with products.

4) Net profit – in throughput accounting, the net profit is simply throughput minus operating expenses.

Looking at 1-4 above, you can see no attempt is made to allocate any overhead cost, so throughput accounting does not meet normal GAAP requirements. It does however raise the possibility of selling products/services at a price which is lower than under normal cost accounting, and it may also be useful for short-term decision making. Below is an example of a profit statements from Burns et al (2013. p. 112), which shows how throughput accounting produces a differing view on costing.

The overall net profit figure is exactly the same, but you can see a much bigger contribution under the throughput method. Arguably, as only material costs (in this example) are totally variable, a report such as the one above is very useful for short term decision-making.

References:

Management Accounting, Burns,Quinn, Warren & Oliveira, McGraw-Hill, 2013 – see burnsetal.com

Hidden costs – what are they?

Opportunity Cost (Photo credit: maxymedia)

The term “hidden cost” is one which we are probably quite familiar – the media like to use if a lot. But what is a hidden cost? Where do these costs hide? Can we avoid them in decision-making? Too many questions to answer in a single post, but let’s start with the term itself.

If you do a google search, you will get many definitions which define hidden costs as a similar concept to opportunity costs. I disagree with such definitions as if you have identified an opportunity cost, then it is not hidden is it? Ok, perhaps I am being a bit unfair here, but to me hidden costs are those which you may not foresee when making a decision. Of course, it’s never possible to foresee all costs when making a decision, but perhaps the hidden costs might emerge if more time is given to the decision – easier said than done in a business scenario.

Take the example of a house purchase decision. This is a big decision in anyone’s life, and we normally take the time to make the right decision on location, size, internal layout, price, amount to borrow and so on. After a few years in the house we might discover we are far from schools or work, or that it is hard to heat the house – these would be hidden costs of our house purchase as we probably did not factor them into our initial decision. There’s a good chance though that we would include such things in a second house purchase decision.

Managers should know the numbers

At the end of June this year, Michael O’Leary from Ryanair was his usual self at the Paris Airshow. He let a few jibes fly at almost everyone. He also signed an order with Boeing for new aircraft, worth around $1.5 billion. Plans for future aircraft purchase were mentioned too and O’Leary compared two possible aircraft – one from Boeing and one from Airbus. While he suggested both were similar aircraft, the Boeing has 9 more seats and he said ‘that’s worth a million bucks’. When I read this , I thought is this just another quip or does we know his numbers well?

So, here are my calculations:

9 seats at average revenue of €70 = €630

Assume four flights per day per aircraft, so 630 x 4 =€2,520.

Finally, assume 360 flying days per year, this gives 360 x €2,520 = €907,200.

Let’s not argue over the rounding, and maybe my sums and assumptions are not correct. But a round €1million per aircraft per annum adds up to a lot of money. So although O’Leary’s rule of thumb may seem like a quip, it seems to be quite a good rough measure. He is an accountant after all!

The power of an infographic

I have written a few posts previously with infographics. I like them. They convey a message in an easy to understand way. Of course, as a management accountant, I would say they may also include some really useful information to help managers (and others) make decisions.

Recently, Dr Stephen Jollands from Exeter sent me this one. It is so clear and it’s message is direct and simple – despite the many complexities within renewables and the environment etc.

US Postal Service – reduced volumes = reduced costs

(Photo credit: Wikipedia)

In February this year, the United States Postal Service (USPS) decided to cease delivering mail on Saturdays. While this may be seen as inconvenient for some personal and business users, in management accounting terms it is probably a simple cost-volume issue.

Mail volumes have fallen globally due to email and other communications media. With falling volumes, a postal service would either have to reduce costs or increase revenues to maintain profits – or keep state subsidies low. Increasing revenues may be difficult given the competition is sectors such as parcel deliveries, which have increased in volumes. It is also difficult to raise postage rates given the political and/or state involvement. So this leave costs, or more specifically cost-cuts, to get things back in balance. Apparently, ceasing Saturday deliveries will save $2 billion annually. You can read more here from The Economist

Money in Formula 1

Following from my last post, I done a little digging around and found a great article in Forbes about the money and brand valuations in the Formula 1 business. Red Bull may the new and hip brand, but Ferrari is viewed as the most valuable. Have a read here