Why do I need to prepare a budget

Photo by Breakingpic on Pexels.com

In my previous post, I mentioned being part of a local voluntary committee, and our efforts to bring a Christmas market to my local town. It’s all going well, but as we near our first year end, it has become apparent to me how important it is for us to plan better for the following year.

Like many voluntary organisations, we are probably still finding our feet. While I keep track of the monies in my role, what I do not have is the full picture of what monies will be spent. To be fair none of us do, as this is the first time we have organised this event and none of us within the organisation have prior experience of such an event. However, a budget is exactly what will bring us together and help us focus for next year. By the end of the Christmas period, we will know what costs we have incurred to host the market and these can be the basis for discussions for the coming year. Then, with a budget in place, we can start to plan for what we need to achieve and of course we can keep a control on things. If you read any management accounting textbook you will see pros and cons of budgeting. To me the biggest advantage of preparing a budget in this small voluntary organisation is that we can all talk from the same page – i.e. the communication value of the budget.

Another cost overrun example

Following from my last post, here is another example of costs and design problems -but this one is a real project. A bridge crossing the Bay Area in San Franciso had an original cost estimate of $250, but the final cost was in excess of $6 billion. This occurred for many reasons, bad cost estimates, politics and the length of time involved. Read the article at the link for full detail – it’s a great example of the cost problems associated with infrastructure projects.

CVP analysis – the effects of too much volume ?

Last summer I again took the car to Europe, using the Dover-Calais crossing. Not too long before I went I read an article about a UK Competition Authority ruling against one of the ferry operators – read here.

One of the operators is (now) owned by euro tunnel, hence the competition ruling. But let’s bring this to basic costs, volumes and profits. The ship I travelled on was almost empty, and as there is so much capacity on the route some operators are being pushed into a loss scenario. Why? Well, think about it for a moment – costs of running a large ferry are probably quite fixed. Prices may be low due to competition, but volume is relatively static. So, lowering price to attract passengers may be a loss maker. Similarly, too many operators may mean smaller passenger numbers for all, driving some into a loss situation.

So, as basic economics may dictate, ultimately one operator will fail as the market will force them out. And remember CVP analysis is based on a subset of the cost curves used in economics.

A $4billion budget trick

While searching the web for some blog material I came across this. It’s a great story about how some US senators played some tricks with various departmental budgets to plug a hole in another.

Hidden costs – what are they?

Opportunity Cost (Photo credit: maxymedia)

The term “hidden cost” is one which we are probably quite familiar – the media like to use if a lot. But what is a hidden cost? Where do these costs hide? Can we avoid them in decision-making? Too many questions to answer in a single post, but let’s start with the term itself.

If you do a google search, you will get many definitions which define hidden costs as a similar concept to opportunity costs. I disagree with such definitions as if you have identified an opportunity cost, then it is not hidden is it? Ok, perhaps I am being a bit unfair here, but to me hidden costs are those which you may not foresee when making a decision. Of course, it’s never possible to foresee all costs when making a decision, but perhaps the hidden costs might emerge if more time is given to the decision – easier said than done in a business scenario.

Take the example of a house purchase decision. This is a big decision in anyone’s life, and we normally take the time to make the right decision on location, size, internal layout, price, amount to borrow and so on. After a few years in the house we might discover we are far from schools or work, or that it is hard to heat the house – these would be hidden costs of our house purchase as we probably did not factor them into our initial decision. There’s a good chance though that we would include such things in a second house purchase decision.

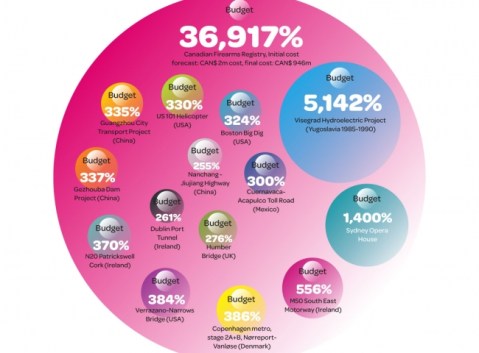

Cost overruns on projects

Here is a great infographic from the February edition of CIMA’s Financial Management. A few Irish projects in there. I think we’re better nowadays, but I may stand corrected on that.

Read the full article at this link:

15 of the world’s biggest cost overrun projects | CIMA Financial Management Magazine.

What is a manufacturing execution system (MES)?

In my former life as a management accountant in industry, I worked in a number of projects which automated either production itself, production planning, or both. A term I was use to at that time was Manufacturing Execution System or MES. So what is an MES and why should management accountants know about them? Well, an advertisement in the November 2011 edition of Financial Management (CIMA’s monthly magazine) prompted me to write about it. AN MES is a system which basically communicates from sales through to the actual making of a product or a the start of a process. An MES may include a sales order module, which would gather customer orders and pass these on to planning modules or directly to process equipment. Typically, an MES will improve a production process as production is scheduled more efficiently and can be monitored for back-logs and jams. Also, an MES will also typically integrate with an ERP system, which means that a businesses systems are fully integrated. According to the advert in the CIMA magazine, Carlsberg (yes the brewer) improved performance in several areas once it used an MES; sales increased bu 1.5%, gross margins up 1.2%, downtime decreased from 28% to 13%, material loss decreased by 1%. All of these translate into increased profitability, which of course is of interest to managers and management accountants. I would argue that understanding how an MES works in a business is a vital piece of kit for any management accountant, particularly if such performance improvements can be made. If you are interested in reading some more, here are two websites I am familiar with which offer MES systems; Kiwiplan and ATS.

In my former life as a management accountant in industry, I worked in a number of projects which automated either production itself, production planning, or both. A term I was use to at that time was Manufacturing Execution System or MES. So what is an MES and why should management accountants know about them? Well, an advertisement in the November 2011 edition of Financial Management (CIMA’s monthly magazine) prompted me to write about it. AN MES is a system which basically communicates from sales through to the actual making of a product or a the start of a process. An MES may include a sales order module, which would gather customer orders and pass these on to planning modules or directly to process equipment. Typically, an MES will improve a production process as production is scheduled more efficiently and can be monitored for back-logs and jams. Also, an MES will also typically integrate with an ERP system, which means that a businesses systems are fully integrated. According to the advert in the CIMA magazine, Carlsberg (yes the brewer) improved performance in several areas once it used an MES; sales increased bu 1.5%, gross margins up 1.2%, downtime decreased from 28% to 13%, material loss decreased by 1%. All of these translate into increased profitability, which of course is of interest to managers and management accountants. I would argue that understanding how an MES works in a business is a vital piece of kit for any management accountant, particularly if such performance improvements can be made. If you are interested in reading some more, here are two websites I am familiar with which offer MES systems; Kiwiplan and ATS.

Reducing costs at the design stage

A CIMA report on the manufacturing sector from August 2010 highlights a number of current issues facing the sector. One of the issues mentioned is making products cost efficient by designing in cost effectiveness at the design stage – and this includes costs of designing in poor quality, just think of the issues with Toyota cars last year. So how can management accountants help at the crucial design stage. According to the report, a number of ways actually. First, the report states that a significant proportion of product costs (up to 80%) are determined at the design stage. Therefore manufacturers will benefit from the management accountant modelling costs for the prototypes or revisiting costs when testing is complete. Another way

A CIMA report on the manufacturing sector from August 2010 highlights a number of current issues facing the sector. One of the issues mentioned is making products cost efficient by designing in cost effectiveness at the design stage – and this includes costs of designing in poor quality, just think of the issues with Toyota cars last year. So how can management accountants help at the crucial design stage. According to the report, a number of ways actually. First, the report states that a significant proportion of product costs (up to 80%) are determined at the design stage. Therefore manufacturers will benefit from the management accountant modelling costs for the prototypes or revisiting costs when testing is complete. Another way

How to prepare an annual Budget

I’m a bit stuck for time just now, so here’s a useful post I found on inc.com recently. It give good advice on setting an annual budget, a cash budget and tips on your first budget if you’re a start-up. Here’s the link: How to Set an Annual Budget.

I’m a bit stuck for time just now, so here’s a useful post I found on inc.com recently. It give good advice on setting an annual budget, a cash budget and tips on your first budget if you’re a start-up. Here’s the link: How to Set an Annual Budget.