The end of low cost air fares?

Over the years, I have used lose cost airlines as examples in several of my blog posts. Carriers like Ryanair have always interested me – whether you love them or hate them they are successful.

A recent article on RTE’s business section gives a good summary of the low cost sector, but also considers how costs have and will increase, leaving no option but to increase fares. You can read the article here.

Increasing fuel costs – Repsol provide interesting approch

With recent events in Ukraine, the world has faced a sharp rise in fuel prices. This applies to individuals and business. Here in Ireland where I live, our government has reduced the taxes on fuels, which in turn reduce the at pump price.

Repsol, a Spanish company has taken an interesting initiative. They have reduced prices of fuel by 10c per litre, but only if you pay using their app Waylet. Thinking as a management accountant, I am thinking this is quite smart on their part. I am guessing, but I would assume that paying via the Waylet app reduces many costs – such as payment processing fees, or cash handling fees for example. Thinking as a manager with a more strategic hat on, maybe Repsol are attempting to make all payments cashless, and this is a way to move more people towards their Waylet platform. Regardless, I would be confident the reduction of 10c in price is compensated by an equal cost saving somewhere.

Management accounting and sustainability

Throughout my professional and academic career as a management accountant/teacher of same, the issue of sustainability has always been something with just made intuitive sense to me. This may be due to my rural background which has instilled an appreciation of all things around me into my ways of working and thinking.

Of course, sustainability is a key issue for business and us all. I recently stumbled upon a CIMA Research Insight report on sustainable development which I had not read previously. The report focuses on the United Nations’ 17 Sustainable Development

Goals (SDGs) and the role of management accounting. Rather than summarise it here, it may be best to read the report yourself, but one quote from within the report really captures the important relationship between business and sustainability. The quote is:

“If business isn’t sustainable then society is at risk. And if society isn’t sustainable then business is at risk.” – Mark Wilson, Group Chief Executive Officer, AVIVA

What a clear and simple quote!

Hidden costs – closing operations

In recent years many operations – both business and public sector – have been closed or reduced in capacity to save costs. Closing an operation is one of the topics I often teach too. When I teach, the basic message is to focus on the fixed costs, and how much can be reduced or eliminated. Of course, some labour costs are increasingly seen as fixed – and this may be a more certain feature in the public sector.There may also be some hidden or unforeseen costs, which are often not included in the analysis. Let me give you two recent examples, both of which are from the public sector.

In recent years many operations – both business and public sector – have been closed or reduced in capacity to save costs. Closing an operation is one of the topics I often teach too. When I teach, the basic message is to focus on the fixed costs, and how much can be reduced or eliminated. Of course, some labour costs are increasingly seen as fixed – and this may be a more certain feature in the public sector.There may also be some hidden or unforeseen costs, which are often not included in the analysis. Let me give you two recent examples, both of which are from the public sector.

In Ireland, the government closed down 139 Garda (police) stations due to economic woes. Most of these closures were in rural areas. The total annual cost saving is estimated at just over €500,000 – see here. This is likely due to the fact that only the only savings were operating costs of the stations e.g. light and heat were the only real costs saved. Police staff and equipment simply moved to another station – where costs may have been incurred to accommodate them. There is a big hidden cost though, which is increased rural crime. While there was probably no money value on this cost in any cost estimates prepared, I’d be quite sure it is higher than closing stations. Recently, the decision to close has been reversed.

A second example comes from Lambeth council in London who closed two libraries – see here . According to a report in the Guardian, the daily security cost is higher than the cost of keeping the libraries open. There seems to have been some protests against the closure of one library in particular, which drove up the costs. This unforeseen cost, if included in the closure decision might have changed things.

A challenge to Ireland’s banks – I’d love to hear your comments

Image (journal.ie)

To this audience I ask two questions

- do you understand short-term versus long-term? If you do, which applies to your decision-making?

- are there any trained management accountants working in banks? I know there are, so read below if you are one of them.

While driving back from Cork recently, I heard a decent sounding lady with six kids telling a story about how a bank was repossessing the house her family rented – it was the Joe Duffy show on RTE Radio 1. The landlord could not afford the loan repayments it seemed and the bank wanted to sell the house. The family worked, and had sufficient income to pay rent into the future. The husband worked in a state-job, so as secure as you could get. She tried to communicate with the bank, but got a “computer says no” type response from the bank. To me, and I am just a management accountant, not a banking expert I could not see the logic in selling the house. Something instinctively told me taking a longer term view is a better choice.

Based on the information she gave during the radio show, when I reach my home I opened an Excel sheet. I checked the rent the lady might be paying – from daft.ie – and then I started to use the simple PMT function in Excel. I made assumptions that the landlord stopped paying the bank loan based on the original house value in 2010; that the bank would allow the lady to take over the mortgage at the present market value of the house and at the present interest rate. I did not adjust for the time value of money. You can see all my workings at this link:

The total time to do the above calculations was about 20 mins. I admit, Excel is not perfect, and I do not adjust for the time value of money – I don’t think it will make things vastly different. To keep it short, if the bank allowed the lady to take over the house as described above, they would gain to the tune of just under €86,000. Based on my simple calculations, the lady could afford to pay this. So, taking a longer term view, the bank (and by definition it’s shareholders) would benefit compared to ditching the house now.

Some further points on costs. I ignore legal costs, as the bank would have to suffer legal costs on either a sale or re-mortgage. But there is a bigger elephant in the room on costs. The lady would be homeless, someone would have to pay this cost – directly or indirectly, and ultimately the state. If I extrapolate the social costs, what is the family (who seemed decent) became homeless, the family fabric was disturbed and the kids turn to crime in the future. How much would this cost in money terms ?

So back to my questions. The scenario I describe above is being repeat all across Ireland. As a person, and an accountant this annoys me. The view of banks seems to be short-term only, driven by profit only. Now don’t get me wrong, profit is good, it creates jobs and investment. But we must not view profit from a short-term perspective. So, to the bankers, give me an answer to the above questions. If you are a trained management accountant, you should be thinking long-term, and if not, don’t think you cannot fail by taking short-term views. As you know banks have failed, as the leading image here should remind you.

A simple definition of management accounting

When some one asks me for a simple definition of management accounting, I typically say “the provision of decision-making information to managers”. This in my view covers all aspects of what a management accountant typically does, be it the provision of financial or non-financial information, short or long term view etc. Of course, some management accountants are also decision-makers, for example when they occupy a CFO role in a large company for example.

I don’t know if I should be surprised or not, but I read an old article from the Irish Times of 22 January, 1971 (by C Power) – a few years (but not many) before my time. The article was giving career advice to budding accountants of that time. I quote:

” A more specialist sector, however, is the cost accountancy field. This is a key area – indeed cost accountants are often referred to as management accountants because of their function of providing accounting information to aid management decisions”

The bit is bold is above is not that dissimilar from my simple definition I guess, with the exception being the maybe narrower word “accounting” as part of the definition. I do like simple definitions, as they often do stand the test of time.

Management accounting during WW1

Image from wikipedia

As you know I’m sure, 2014 was 100 years since the outbreak of the Great War, or World War 1 as we know it today. Myself and a colleague were lucky enough to do some research on how management accounting was affected by the war. I will summarise our work here, but you can find the full paper here.

We studied how the war affected management accounting at Guinness – yes the world-famous stout. I had already carried out some research at Guinness, so I was aware that even before 1914 they had a relative complex management accounting system. They were quite good at allocating costs to various cost centres.

As the war broke out, the accountants and managers initially viewed it as a short-term event. It became apparent soon enough that would not be the case. Thus, Guinness started to view additional costs (such as extra insurance costs) as normal costs and allocated them to various cost centres. For example, if Guinness shipped to Liverpool or London, the freight costs were normally charged to the receiving depots owned by the company. With the war in full swing, the additional insurance costs for these trips was also allocated to the depots.

The company made other changes too, but the above example is a good case of existing practice being modified to deal with new business issues- something which management accountants still do a lot of today.

What is life cycle costing?

You may have seen the typical product life cycle graph in your previous studies (see left). The basic idea is that sales in money and volume increase over time, but gradually tail off as the product comes to the end of its cycle.

You may have seen the typical product life cycle graph in your previous studies (see left). The basic idea is that sales in money and volume increase over time, but gradually tail off as the product comes to the end of its cycle.

When we think of management accounting and product costing, we are generally looking at short-term costs, and not all costs a product may incur over it’s life cycle. For example, there may be advertising costs to boost sales of mature products, costs of product development or even remediation/disposal costs. Life cycle costing include all costs of a product or service from design to end-of-life. All recurring and once-off costs are included over the entire life cycle. These costs can then be compared with expected revenues to determine if a product is profitable or not.

To give you an example, consider the drug development life cycle. It may take many years and cost €billions to bring a drug to market (see here for example, which depicts the process at Bayer), before a single euro in revenue is earned. Then, there are the on-going manufacturing costs. Perhaps the drug has side effects, and needs some improvement during its life. And perhaps as the drug ends its life, there may be costs in dismantling purpose-built manufacturing facilities. Taking all these items (and more no doubt) a drug company can consider if a particular drug is profitable.

What is lean accounting?

Defining lean accounting is a bit odd to me, as I don’t really buy the idea that there is a technique called “lean accounting”. Having said that, there is definitely a concept called lean manufacturing. In a nutshell, lean manufacturing implies three concepts – pull, flow and waste reduction. Pull means product is produced (or pulled) according to customer demand. Flow means product moves through a facility as efficiently as possible and no delays. Both of these should imply waste reduction.

So what does this mean for accounting. Well one thing is inventory reduction. Another may be capital investment to get things working well. Both might put accountants off! But rather than me rattle on, here is a very nice article from Forbes which explains lean accounting and some issues.

What is throughput accounting?

Throughput accounting is an alternative to traditional internal cost reporting. It stems from the Theory of Constraints, which I won’t detail here, but essentially this theory suggests an organisational can best achieve its goals (e.g. profit) by maximising it use of a constraining resource. A constraint could be machine capacity for example, and by maximising throughput on the constraint profit is maximised. To report on throughput, a new accounting approach is required, called throughput accounting:

1) Totally variable costs – this means a cost which is incurred only when a product/service is created. This often means only material costs. Labour costs are not totally variable, as employees are typically paid regardless. Some transportation or subcontracting costs may be totally variable. All overhead costs are not totally variable.

2) Throughput – this refers to revenue less totally variable costs. Contribution using throughput accounting is likely to be higher.

3) Operating expenses – this refers to all costs other than totally variable costs. Operating expenses are not distinguished into categories such as fixed or variable, or allocated to products in any way i.e they are similar to period costs, as they are costs which are more

associated with the passage of time than with products.

4) Net profit – in throughput accounting, the net profit is simply throughput minus operating expenses.

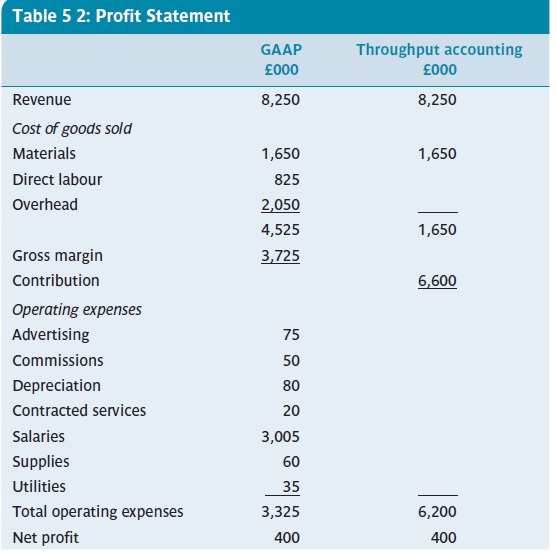

Looking at 1-4 above, you can see no attempt is made to allocate any overhead cost, so throughput accounting does not meet normal GAAP requirements. It does however raise the possibility of selling products/services at a price which is lower than under normal cost accounting, and it may also be useful for short-term decision making. Below is an example of a profit statements from Burns et al (2013. p. 112), which shows how throughput accounting produces a differing view on costing.

The overall net profit figure is exactly the same, but you can see a much bigger contribution under the throughput method. Arguably, as only material costs (in this example) are totally variable, a report such as the one above is very useful for short term decision-making.

References:

Management Accounting, Burns,Quinn, Warren & Oliveira, McGraw-Hill, 2013 – see burnsetal.com

Speed cameras business

In July this year (2013), I read an interesting brief news report about a speed van operator in Ireland. Yes, we all hate these guys, but the article made me realise this seems like a good business to be in – even if you are hated by motorists. According to the article, the GoSafe consortium makes a profit of almost €50,000 per week or €2.5m per year. It has almost €11m debt and is contracted to provide 6,000 hours per month to the Irish state. The article notes that at least one motorist per hour is caught speeding. I don’t know the ins and outs of the contract, but if the company makes a profit of €2.5m annually, even if it does pay out some dividends, the debt owing could be paid down quickly it would seem. The management accountant in me would really like to know what is the breakeven number of speeding motorists per day! You can read more at this link: http://www.rte.ie/news/2013/0720/463662-speed-vans/

A great reporting tool from Excel – PowerMap

As you might know from some of my previous posts, I really like concise presentation of information. The infographic is one of my favourites. Graphical reporting is always great, and managers tend to really like it – it simple, conveys trends, and it’s not boring accounting numbers.

I read a piece on CIMA Insight about a new add-in for Excel 2013 called GeoFlow, or more correctly PowerMap. You can read the full article here. The add-in uses Bing Maps (from Microsoft) and you can plot up to a million rows of data against a map. You can also plot date data, so you could for example see how sales have trended over time on a map. The data can be presented in 3D format, as bubbles, or as a heat map. This tool will certainly create really cool business reports.

Managers should know the numbers

At the end of June this year, Michael O’Leary from Ryanair was his usual self at the Paris Airshow. He let a few jibes fly at almost everyone. He also signed an order with Boeing for new aircraft, worth around $1.5 billion. Plans for future aircraft purchase were mentioned too and O’Leary compared two possible aircraft – one from Boeing and one from Airbus. While he suggested both were similar aircraft, the Boeing has 9 more seats and he said ‘that’s worth a million bucks’. When I read this , I thought is this just another quip or does we know his numbers well?

So, here are my calculations:

9 seats at average revenue of €70 = €630

Assume four flights per day per aircraft, so 630 x 4 =€2,520.

Finally, assume 360 flying days per year, this gives 360 x €2,520 = €907,200.

Let’s not argue over the rounding, and maybe my sums and assumptions are not correct. But a round €1million per aircraft per annum adds up to a lot of money. So although O’Leary’s rule of thumb may seem like a quip, it seems to be quite a good rough measure. He is an accountant after all!

What does ‘cost’ mean?

If we look at a management accounting text book such as the one by Burns et al (self promotion, sorry), the term cost is defined as follows:

“the monetary value of the resources forgone or sacrificed in order to achieve a specific objective such as acquiring a good or service”

And, if we continue to read their chapter on costs (or indeed a similar chapter in any other management accounting text) we’ll find that costs can be classified in many ways – fixed, variable, mixed, product, period, relevant are just some classifications commonly used. I recently watched two documentaries on BBC television which portrayed the different meanings and uses of the word cost. I’ll summarise them below.

The first example is from a documentary called Inside Claridge’s – Claridge’s is a up-market hotel in London. In the episode I watched, the hotel was being decorated for Christmas. The decorations inside and out were quite fabulous, and the Christmas tree was commissioned from a custom designer. The programme narrator asked the hotel manager how much the decorating cost. His reply: “How much does magic cost”. A great answer I thought. To try to convert this to management accounting speak, I would translate the answer as “That’s not a relevant cost, the decision is made”.

Fault (Photo credit: orkybash)

The second example was a documentary on BBC Four on living near an earthquake zone or fault lines. One seismologist spoke about a complex underground monitoring system, which could sense earthquake vibrations and give warnings (via sirens or signs) to residents in cities like Los Angeles and San Diego. The system would cost in excess of $100 million, and give enough time to do things like shut down nuclear reactors or close-up an open wound on a hospital operating table (the seismologist’s words, not mine). I was thinking $100 million, that’s a lot. The seismologist then quickly noted that the economic output of California is in the order of $200 billion per annum. This makes the cost look a lot smaller, given that large earthquakes probably are a once in a lifetime event.

Kindle Fire breaks even – but profits elsewhere

Image via CrunchBase

I have written a few posts before on breakeven, but here is a great example of how businesses are prepared to accept not making money on some products, for the sake of others. In October 2012, Amazon launched its Kindle Fire tablet and its Paperwhite e-reader in the UK and other European countries. The Kindle Fire retails at about £150, which is probably less than half the price of an iPad and about £100 cheaper than an iPad mini. In an interview with the BBC , Amazon’s boss Jeff Bezos said the company sells its hardware at cost i.e. they breakeven. This may explain the cheaper price of the Kindle Fire compared to the iPad. However Amazon earn profits on Kindle book sales, Kindle book rentals and its Prime service. In contrast, Apple have noted they breakeven on services such as iTunes and make profits on their hardware,