The “cost” of refunds and claims – a management accounting view.

In recent years in Ireland, business insurance costs have been increased dramatically due to increasing volumes of claims against them. In some cases, the costs have increased so much that the businesses have simply closed. This post is more about the smaller claims, claims for refunds or costs incurred because a product or service was not up to scratch.

I will use Ryanair as the example here. Despite all the criticisms levelled against it, it remains one of my favourite airlines. They run a tight operation and keep costs to a minimum. They also do not payout refunds or claims unless they have to, this is the fun part for me. In a recent Irish Times article, there are details of a customer claiming €222 for taxi fares incurred due to a Ryanair mistake. The company fought it, but the passenger pursued through a small claims court and got their money refunded. Fair play to the passenger.

Recently I was subject to a delay on a Ryanair flight from Bristol. Some passengers, those who were UK citizens I later found out, were offered £5 refreshment vouchers. I was not, and followed up. To be fair to Ryanair they said if I could produce a receipt, they would refund me.

Now the accounting part. In both examples above there are a lot of costs already incurred in having a customer service function to deal with such issues. Let’s deem these as sunk costs. Once a claim is initiated, then I think we could see the situation as an instance of activity based costing perhaps. In my own case, I sent three emails and I can guarantee the cost of dealing with me was way more that the price of a cup of coffee I was seeking to claim. In the case of the passenger taxi fares, costs of engaging solicitors by Ryanair would have far exceeded the cost of the refund had they simply paid it based on the passengers receipts.

The point I am trying to make is that while I fully agree that firms should not just pay refunds without any basis, there is likely some value at which it costs more to defend a refund claim than simply pay it – with vouched receipts of course, not like me and my coffee. But, if you are not getting satisfaction from a company if you feel you should get a refund, apart from legal options, you can always waste their time a little and get some satisfaction that way.

Reasonable business expenses

I am sure you have read or heard stories in your country about political leaders or CEOs spending large amounts of money on expenses – hotels, meals etc. I have read a lot of such reports in recent weeks and just wanted to give a view on it.

To me, and much of this is based on experience, the first principle to me is simple – no receipt or invoice, then any expense should not be reimbursed. Doing this sets a basic principle which is easily understood. I have heard some comments over the years that there is a cost is running an expenses reimbursement system, which may exceed the value of the expenses, so why bother. This may be true in some cases, but I do not agree.

A second principle to me is a basic accounting one – business expenses only. The idea of say using a business credit card for personal lunches or whatever at a weekend goes against the entity principle. This principle means only items for the business should no part of the accounting for that business.

Third, the expense, once for the entity should be reasonable, but what is reasonable? This is where common sense must apply. Let’s take hotels as an example. It may be that a room for €100 per night is ample for any business person, but in some cities this may not be enough for even a basic hotel. But, if I were to say €1000 per night, you would probably think that is a bit too much. Of course you may have read reports of business leaders and political figures spending many thousands of Euro/Pounds/Dollars per night on hotels. Is this reasonable? Personally I do think some of these people could be a bit more modest!

Costs of the Irish president

The gentleman above is Michael D Higgins, the Irish president – of course he is well known to me and other Irish people, but just for the benefit for others you might read my blog.

The gentleman above is Michael D Higgins, the Irish president – of course he is well known to me and other Irish people, but just for the benefit for others you might read my blog.

In October, there will be a presidential election and Michael D is up for a second term of office most likely. In recent months there has been a lot of media attention as of how much the presidential office costs to run. The office does not have much power, but is a great representation of Ireland as a country. According to the presidential website, the cost is about €3.6 million per annum. The vast majority of this consists of staff and travel costs. However, in various media outlets I have heard numbers being mentioned about the costs of the police officers and army associated with the presidential office. At the link above, these count for about €250,000 in 2017.

So what you say! Well, are these costs relevant to the cost of the presidential office? Would they be avoided if the office ceased to be? I doubt it, as the army and police would be put back to their normal duties. So this is a simple example of costs not bring relevant, and thus they probably should be excluded from any comments or analysis. I would guess too that the kind of simple analysis I have done here might be applied to many other political figures. What is probably most important though is that the costs of the office of the Irish president are now being discussed and new controls and checks may result – which is a good thing.

Activity-based costing in healthcare

Photo by Pixabay on Pexels.com

When I teach Activity-based costing (ABC), one of the example sectors often given to students is healthcare. Just in case you don’t know, ABC is a costing technique which allocates cost to products or services based on resources used by the product or service. If you think about healthcare, even in a standard medical procedure, no two patients are the same and use more or less drugs, time, hospital resources etc. Thus ABC appears useful – one patient may use more resources than the other and so cost more.

Of course, healthcare systems around the world vary. Some are fully funded by taxation, some are fully private. In Ireland, the system is mainly a public one, but unfortunately, it is not great in terms of access to treatment. So, if you can afford it, you can have private medical insurance (US style, but less costly) and this gives you more options. With this in mind, here is my recent experience which made me think about ABC and write this post.

Last year, I spent 11 days in a hospital for some heart surgery. Thankfully all is well. I am lucky enough to have health insurance. About three months post-surgery, I received an advice from my insurer stating how much the hospital had been paid – about €25,000. Phew, thankfully I did not have to find the cash for that! The advice was interesting in that showed little sign of ABC techniques – and as my hospital was one of the more advanced and modern I would have expected it to use ABC, to be honest. What the advice showed was a charge per day, with this charge being higher for two days in intensive care. Otherwise, there is little else. Unfortunately for me, I had some complications which required more drugs and attention from staff, so I took up more time and resources than some of my hospital mates (trust me, you make some good friends in hospitals). But this is not reflected in the cost. I suppose on balance things work out for the hospital and it may not matter, but to me, this simple example is a prime case where ABC could be used easily. If it were, then maybe health insurance costs would be a lot less in some cases – but that’s a whole other debate.

Having said all of the above, research on ABC use shows it is often less than 20% in practice. So maybe I should not be expecting its use in my hospital at all.

The cost of medicines – a quick view

I’ve been quiet recently on here due to some illness. While I’ll and having some time on my hands I began to ponder the cost of medicine and where I live ( Ireland ). I know we are one of the more expensive places to buy medicine in Europe, but here I’m not going to refer to any price indices or similar. Instead I’m going to try to quickly break down the costs of doing business in two countries – Ireland and Spain – to explain price differences. A business manager might do this regularly to gauge the competition. To give an example of the price difference, I know that a common prescription pain killer costs €26 in Spain versus €42 in Ireland. Some medicine I use myself costs about €12, versus €23 in Spain. And just tonne clear, these two examples are for identical nongeneric medicines.

The first is taxes. I found that most medicines in Spain have 4% VAT, whereas most in Ireland are at 0%. So we can rule this out. Second, a tax consultant in Spain told me that to purchase a pharmacy in the city I stayed in would cost about €2 million. This is due to limits on how many pharmacy licences there are. This cost results in high depreciation from an accounting perspective, and is similar to Ireland. Third, by my guess, all other costs like labour, rent, light etc are cheaper in Spain, probably 10-50% less. So this leads me to one remaining thing – profit margins. The profit margin would be spit between the pharmaceutical company, a distributor and the pharmacy itself. Without insider information, it is very hard to know what these margins are. Having said that, they must be a large explanatory factor for the price difference.

And for the fun, to give a more marked price difference. I recently saw a TV programme on the cost of medicine in the US. It not the cost of a monthly supply of insulin at $900. This was quite unaffordable for pensioners on a low income. Many who are near the Canadian borders drive across to Canada, where the price of the same product is CAD$ 120.

Of course, I’m doing a quick and dirty, non- scientific analysis here. But business is full of gut instinct and similar, and my experience and gut tells me profit margins are a huge explainer for medicine price differences between countries.

Food supply chain and accounting

In my daily work as an accounting academic, income across many papers and articles which explore the broader role of accounting in society and out daily lives. Lisa Jack from the University of Portsmouth writes about the role of accounting in the food supply chain. This is a very interesting area, as information on costs and margins is crucial in the food sector. She has just published an article on the recent contamination of eggs in some

European countries – you can read it here. It gives a good overview of how accounting is entwined in this and other food issues, and how it could help.

Understanding costs is key

I probably don’t need to explain the title of this short post, it’s quite obvious. Any business needs to appreciate all costs of the products or services it delivers.

- In past years, manufacturing has shifted to some degree to lower cost locations such as China, and the Foxconn relationship with Apple is a classic case. In the case of a product like an iPhone or iPad, it’s quite easy to see how the assembly costs are probably the higher component, and as they are small, distribution costs are low. But as a recent article in Forbes shows, transport costs are often a reason for manufacturing being close to market. In the article, there is mention of Foxconn planning to $10 billion plant in the US to build larger displays – for say 60 inch TVs. The article notes that the cost of capital in the US is similar to anywhere else, and labour costs and relatively low, although higher than China. However, the transportation costs would be much lower for such larger displays and thus it makes sense to build a new plant in the US.

Bad PR and avoidable costs at United Airlines

Image from Bloomberg.com

Recently, it seems United Airlines got themselves into a bit of a bad public relations scenario by ejecting passengers (with force) from a domestic US flight. I’ve never used United and based in this, I never will, as it seems they commonly overbook flights.

First, in the age of technology we live in, how the hell a system allows overbooking I cannot fathom. Maybe if a smaller replacement aircraft transpired in an emergency, I can understand, but this would not be an overbooking issue.

You can read an article about the event at the link above, but here’s a brief rundown:

- United over book

- They look for four volunteers

- They offer $400, then $800

- Nobody volunteers

- They forcibly remove four passengers

And all of this to get their own crew to a location for the next day – this alone says a lot about their ability to manage the business, not having a standard way to get staff, or reserving x seats for staff.

Back to management accounting, and we know that an avoidable cost is one which can be eliminated by not doing something e.g. close a production line. We also know that in the long term, all costs are avoidable. So what about the United story. Well, one thing that will no doubt happen is a string of expensive law suits – and I personally hope United get screwed. This is an avoidable cost, and surely are the costs associated with the apparent regular overbooking. I’d even have a wild guess that it may have been cheaper to charter an aircraft for the staff than what this will ultimately cost United. Even $5000 a passenger to entice volunteers would be cheap too, or maybe $50000. Regardless, United need to find a long term solution to avoid such costs. They have apparently now increased the offer to passengers to $10,000 to give to give up their seats.

Some insights from IAG

IAG, or the International Airlines Group, is the the parent of Aer Lingus, British Airways and Iberia. In my university, we were lucky enough to have their CEO, Willie Walsh, speak to us before Christmas.

IAG, or the International Airlines Group, is the the parent of Aer Lingus, British Airways and Iberia. In my university, we were lucky enough to have their CEO, Willie Walsh, speak to us before Christmas.

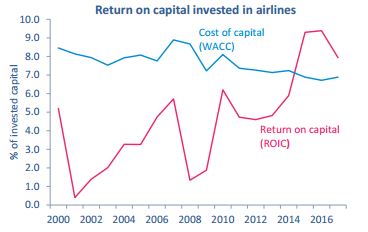

Some things he mentioned are relevant to this blog, and of course interesting. One thing Mr Walsh noted was how only in recent years has the airline sector actually made a return on capital. This must be attributable in some way to a focus on cost by the sector in recent years. The chart below from IATA shows what I mean. As you can see, the cost of capital was higher than the return until 2014.

As my last post indicated, a focus on cost and efficiency has been a feature of the airline sector in recent years. To give another example, Mr Walsh cited an example of using two larger aircraft on a route without a loss in passenger capacity. So fuel, crew and capital cost all decrease in such a scenario. In addition, it freed up a slot at London’s Heathrow airport, which can then be used to generate more revenues.

Unbundling costs at low cost airlines

A few weeks ago, I read a nice article in The Telegraph by David Millward on one of my favourite topics, airlines and  all things to do with airports – I was born close to Dublin Airport and it was a big part of my growing up.

all things to do with airports – I was born close to Dublin Airport and it was a big part of my growing up.

Anyway, many of us have witnessed the phenomena of low-cost airlines emerge of the last 20-30 years, and as an accountant it’s the constant actions to reduce costs that amaze me. As Millward said in his article, one of the things that airlines have done is unbundle. This means you get the basic fare from origin to destination for as low as possible. If you want more you pay more. This is fine by me, on a shorter flight, but now as longer-haul low-cost carriers appear I am not sure – I have no experience yet, so I dare not say. The low-costs have of course eaten into some of the legacy carrier market, but they have also expanded the market by making flying more accessible. Millward suggests that the low-costs have by now probably stripped out all they can to reduce costs, but the legacy carriers can do more – if they wish. I read another article recently which mentioned how WestJet, a low-cost transatlantic carrier remove the in-flight screens to save 500 kg in weight and thus save fuel. They replaced the screens with a wi-fi system and the BYOD idea – most people have their own device on-board anyway. Surely such simple steps could be taken by any carrier.

My favourite sport and accounting!

Probably my favourite (spectator) sport is motor cycle road-racing. There aren’t too many places it still happens – doing 180mph on public roads is not for everyone – but thankfully it still happens here in Ireland, the Isle of Man (IOM) and a few other places.

Probably my favourite (spectator) sport is motor cycle road-racing. There aren’t too many places it still happens – doing 180mph on public roads is not for everyone – but thankfully it still happens here in Ireland, the Isle of Man (IOM) and a few other places.

The IOM TT is probably the pinnacle of road-racing – it’s two weeks of fund each June. imagine my delight when I read an article featuring news on the 2016 TT and creative accounting! The article notes the number of TT visitors for 2016 to be similar to 2015 – based on data from the IOM government. The article also suggested a revenue of £738 per visitor for the economy, based on this same data. In the comments beneath the article, the fun starts.

One comment notes:

“This year’s TT races in June brought a £4.1 million benefit to the island’s exchequer, according to government figures just released.” OK, so that is the claimed revenue, now let’s see the total costs. And by total, I mean the total cost to the island not just the cost of TT preparations. How much for a fatality or serious injury involving medevac? How much for the road closures and effects on businesses as well as the public? These are real costs and the list goes on.

Another states:

I note the total expenditure of £738 pp is not broken down into for example travel costs and monies spent on island. Therefore that figure is meaningless If the figures of £31.3M, £22.5M and £4.1M are based on the £738pp they are also meaningless. Creative accounting it is for sure. In addition, if the government can come up with a figure for the benefit to the island they must be in possession of all costs, such as DOI, medical, policing, helicopters etc. So why do they never produce such figures?

These two sharp commentators highlight many things -the subjective major of accounting, where costs and revenues are attributed, and what are the relevant costs, for example. I’ll be using this example in my teaching at some future point.

Break even for a vineyard.

I read a nice article in the Financial Times recently on the cost of buying a vineyard. The article is investment focused, but mentions that given costs of production, wine prices and annual sales in bottles, the investment will breakeven in a few years – meaning the investment is recouped. If you have studied management accounting, you’ll be aware this not breakeven in the way you many have learned it – fixed cost/contribution per unit. It is not very different though. In essence, the investment is regarded as a fixed cost, with the contribution per unit being the annual contribution which can be made from sales of wine in a year. It’s not a perfect measure, but a good enough rule of thumb to help make an investment decision.

I read a nice article in the Financial Times recently on the cost of buying a vineyard. The article is investment focused, but mentions that given costs of production, wine prices and annual sales in bottles, the investment will breakeven in a few years – meaning the investment is recouped. If you have studied management accounting, you’ll be aware this not breakeven in the way you many have learned it – fixed cost/contribution per unit. It is not very different though. In essence, the investment is regarded as a fixed cost, with the contribution per unit being the annual contribution which can be made from sales of wine in a year. It’s not a perfect measure, but a good enough rule of thumb to help make an investment decision.

Charities as businesses?

In recent weeks, the Irish media has revealed yet another charity mis-using funds – this time the founders used a lot of the charity monies for personal purposes.

In recent weeks, the Irish media has revealed yet another charity mis-using funds – this time the founders used a lot of the charity monies for personal purposes.

Regulation of charities in Ireland is not as good as it could be – we have some legislation waiting to be enacted since 2009 as far as I know. But laws cannot prevent what happens within an organisation from happening; they can only penalise after the event.

So what bugs me? Well, the title of this post really – it is something I picked up from the print media in recent weeks. I am sure I have said somewhere on this blog that accounting is the language of business, so what about accounting for charities? My own opinion is that charities must have proper accounting, and there are accounting standards already in place for charities. But I often wonder should we be careful and not allow charities to become too much like a business? For example, we should be using accounting in charities to drive efficiencies, not necessarily monitor revenue and costs like in a business. Nor should we be using accounting just to get funding for a charity. In short, what I am trying to say is that we need to be careful and try to not let accounting (and other commercial sector notions) detract from what a charity should be.

Hidden costs – closing operations

In recent years many operations – both business and public sector – have been closed or reduced in capacity to save costs. Closing an operation is one of the topics I often teach too. When I teach, the basic message is to focus on the fixed costs, and how much can be reduced or eliminated. Of course, some labour costs are increasingly seen as fixed – and this may be a more certain feature in the public sector.There may also be some hidden or unforeseen costs, which are often not included in the analysis. Let me give you two recent examples, both of which are from the public sector.

In recent years many operations – both business and public sector – have been closed or reduced in capacity to save costs. Closing an operation is one of the topics I often teach too. When I teach, the basic message is to focus on the fixed costs, and how much can be reduced or eliminated. Of course, some labour costs are increasingly seen as fixed – and this may be a more certain feature in the public sector.There may also be some hidden or unforeseen costs, which are often not included in the analysis. Let me give you two recent examples, both of which are from the public sector.

In Ireland, the government closed down 139 Garda (police) stations due to economic woes. Most of these closures were in rural areas. The total annual cost saving is estimated at just over €500,000 – see here. This is likely due to the fact that only the only savings were operating costs of the stations e.g. light and heat were the only real costs saved. Police staff and equipment simply moved to another station – where costs may have been incurred to accommodate them. There is a big hidden cost though, which is increased rural crime. While there was probably no money value on this cost in any cost estimates prepared, I’d be quite sure it is higher than closing stations. Recently, the decision to close has been reversed.

A second example comes from Lambeth council in London who closed two libraries – see here . According to a report in the Guardian, the daily security cost is higher than the cost of keeping the libraries open. There seems to have been some protests against the closure of one library in particular, which drove up the costs. This unforeseen cost, if included in the closure decision might have changed things.

Going green in your house is expensive

In this post, I am having a bit of a go at the costs of material and devices that I would label as “eco” – things that are environmentally friendly and sustainable. I try too to give an answer.

Have you ever noticed how some Eco items cost more than, shall we call them traditional items? For example, eco building materials like some insulations are much more costly than the traditional materials. Or more efficient appliances such as heating boilers cost more. What bugs me a little is, if our goal to is to reduce energy consumption, reduce CO2 or live more sustainably, then why are many things that could helps us so costly?

Two reasons come to mind as a management accountant. First, there may have been some capital costs incurred by manufacturers to produce newer and more sustainable products, which are included in the price. These costs may decrease over time as economies of scale creep in. A second reason is that although the costs may be higher, there may be savings to take into account. For example, an certain insulation maybe be twice the cost, but it can seriously reduce your heating bills over the several decades.