What is throughput accounting?

Throughput accounting is an alternative to traditional internal cost reporting. It stems from the Theory of Constraints, which I won’t detail here, but essentially this theory suggests an organisational can best achieve its goals (e.g. profit) by maximising it use of a constraining resource. A constraint could be machine capacity for example, and by maximising throughput on the constraint profit is maximised. To report on throughput, a new accounting approach is required, called throughput accounting:

1) Totally variable costs – this means a cost which is incurred only when a product/service is created. This often means only material costs. Labour costs are not totally variable, as employees are typically paid regardless. Some transportation or subcontracting costs may be totally variable. All overhead costs are not totally variable.

2) Throughput – this refers to revenue less totally variable costs. Contribution using throughput accounting is likely to be higher.

3) Operating expenses – this refers to all costs other than totally variable costs. Operating expenses are not distinguished into categories such as fixed or variable, or allocated to products in any way i.e they are similar to period costs, as they are costs which are more

associated with the passage of time than with products.

4) Net profit – in throughput accounting, the net profit is simply throughput minus operating expenses.

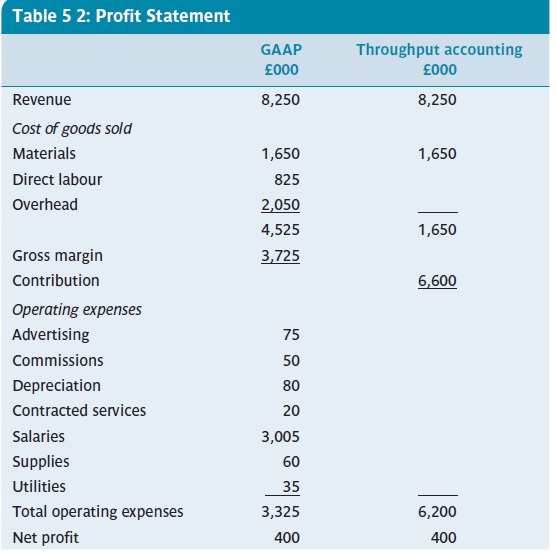

Looking at 1-4 above, you can see no attempt is made to allocate any overhead cost, so throughput accounting does not meet normal GAAP requirements. It does however raise the possibility of selling products/services at a price which is lower than under normal cost accounting, and it may also be useful for short-term decision making. Below is an example of a profit statements from Burns et al (2013. p. 112), which shows how throughput accounting produces a differing view on costing.

The overall net profit figure is exactly the same, but you can see a much bigger contribution under the throughput method. Arguably, as only material costs (in this example) are totally variable, a report such as the one above is very useful for short term decision-making.

References:

Management Accounting, Burns,Quinn, Warren & Oliveira, McGraw-Hill, 2013 – see burnsetal.com

What cost can you sell at?

Factory (Photo credit: howzey)

In this post, I recount a conversation I had with a great mentor some years ago. It questioned my notion of what costs are relevant and how to set prices once a plant/factory is not at full capacity.

In a factory ( or any business perhaps ) when there is free capacity we can start to look at the make up of costs a little closer. Traditionally, management accounting would suggest we should at least cover all variable costs in the selling price. But think about it like this – if we have spare capacity, then perhaps the only additional cost is the material cost. Let’s assume we have a machine with a full crew, but not at full capacity. The fixed costs of the machine are just that – fixed, and we cannot avoid them. The labour costs are in effect fixed too, as workers will be paid. So, in this case, only the material costs are relevant. And this, any selling price above the material cost contributes to profit.

Yes, there may be many simplistic assumptions in the above. However, it made me think back then and I always give this example to my students. It is of course an example of throughput accounting, which I will mention next week.

Related articles

Anyone can call themselves an accountant

Accountant upstairs ↑ (Photo credit: jah~)

Yes it’s true, anyone – in Ireland at least – anyone can call themselves an accountant. And, this has been the case for as long as I have been an accountant. I was reminded of this recently by an article in the Irish Times. To quote from the article:

“Don’t fret, because no qualifications are necessary to trade as an accountant. Anybody can open up a practice, no matter how innumerate they may be – there are no absolutely restrictions on the use of the term “accountant”. Remarkable, isn’t it?”

I guess it is remarkable. Yes, there are professional accounting bodies whose members must pass examinations and keep their training up to date. And yes, to be an auditor you must generally be a member of such bodies. But after that anyone can claim to be an accountant. As noted in the Irish Times, even an upcoming review and consolidation of Irish company law has failed (as yet) to include a provision of who can use the term accountant.

Related articles

- So, you think you are an accountant? (irishtimes.com)

Hidden costs – what are they?

Opportunity Cost (Photo credit: maxymedia)

The term “hidden cost” is one which we are probably quite familiar – the media like to use if a lot. But what is a hidden cost? Where do these costs hide? Can we avoid them in decision-making? Too many questions to answer in a single post, but let’s start with the term itself.

If you do a google search, you will get many definitions which define hidden costs as a similar concept to opportunity costs. I disagree with such definitions as if you have identified an opportunity cost, then it is not hidden is it? Ok, perhaps I am being a bit unfair here, but to me hidden costs are those which you may not foresee when making a decision. Of course, it’s never possible to foresee all costs when making a decision, but perhaps the hidden costs might emerge if more time is given to the decision – easier said than done in a business scenario.

Take the example of a house purchase decision. This is a big decision in anyone’s life, and we normally take the time to make the right decision on location, size, internal layout, price, amount to borrow and so on. After a few years in the house we might discover we are far from schools or work, or that it is hard to heat the house – these would be hidden costs of our house purchase as we probably did not factor them into our initial decision. There’s a good chance though that we would include such things in a second house purchase decision.

Product development and advertising costs

It’s probably fairly obvious that product development costs affect the overall profitability of any product. Some products like drugs and new technology incur huge development costs. New technology, at least at the consumer end, often incurs huge advertising and promotion costs too. And simply, if sales are not sufficient, then losses occur.

As an example, consider a report from the Irish Times on Microsoft’s efforts in the tablet market.

“Microsoft’s Surface tablets have yet to make any profit as sputtering sales have been eclipsed by advertising costs and an accounting charge, according to the software company’s annual report.

The two tablet models, introduced in October and February to challenge Apple’s popular iPad, have so far brought in revenue of $853 million, Microsoft revealed for the first time in its annual report filed with regulators yesterday.

That is less than the $900 million charge Microsoft announced earlier this month to write down the value of unsold Surface RT – the first model – still on its hands.

On top of that, Microsoft said its sales and marketing expenses increased $1.4 billion, or 10 per cent, because of the huge advertising campaigns for Windows 8 and Surface. It also identified Surface as one of the reasons its overall production costs rose.

The Surface is Microsoft’s first foray into making its own computers after years of focusing on software, but its first attempts have not won over consumers. By comparison, Apple sold almost $24 billion worth of iPads over the last three quarters.”

(Above is copyright of Irish Times/Reuters)

Data analytics – the human input

English: Apple director Steve Jobs shows iPhone (Photo credit: Wikipedia)

Big data is a big thing in the management accounting practitioner world, and in the professional journals too. I have previously written some posts on what big data is (see for example, here and here) and I have noted that humans are still needed to interpret data. Here’s a great example, below. Before I start, just keep in mind what I always say to my students about technology – technology within computing devices is essentially dumb, it is nothing more that a series of 0 an 1 which do exactly what we program it to do.

This post from CSO outlines how good analytic is essential. It cites an example of an analysis of social media to predict trends in the US unemployment rate. The analysis used twitter feeds and other social media. It attempted to identify key words such as “jobs” and “unemployment”. A huge spike in the number of tweets appeared. Why? Steve Jobs had just died, so the word “jobs” was all over social media. As a human, we can easily distinguish the meanings of words, but an automated analysis or word collecting tool cannot. I believe management accountants have a key role to play in such sense-making of business big-data – after all we know the business quite well.

Management accountant’s travelogue – part 3 – to toll or not to toll?

(Photo credit: Wikipedia)

As I drove through France and Spain on my holiday, I thought about the tolls one must pay (on most) motorways. I was thinking how do they set the prices of these tolls? Of course, public infrastructure like motorways is often now financed by a combination of public and private investment. Regardless of the investment type, can you imagine how tricky it is to pitch a price for a motorway toll. If it’s too high, less will use it (M6 Toll in the UK) and costs take much longer to be recouped. Set it too cheap and it floods with traffic, which in turn eventually results in less users, and that equals less money. Should the price be set with future investment and on-going maintenance in mind. Should it be a social good with a very low price – but then where will the money come from for re-investment? Lots of questions here, but I hope you can see a lot of management accounting is behind these decisions. I would imagine getting the initial price correct is the toughest part. Nowadays though, I am sure there are plenty of modelling tools to help toll operators and governments.

Management accountant’s travelogue- part 1 – free ferry trips

(Photo credit: Wikipedia)

Sorry about the somewhat cheesy title ! This summer, I spent about 3 weeks on a driving holiday in France and Spain. I love driving to Europe – no airports, luggage limit is a much as you can carry in your car, and you can stop when you want where you want. I drove just over 3,000 miles and stayed in some beautiful places. During my journey, the old business brain was not completely switched off so I’d like to share some things I noticed and thought about. Of course, they will be related to management accounting one way or another.

The first thing I noticed was that the ferry trip to France gave us a free trip to the UK. A free something is nothing new – you can lots of examples of free products, two for three deals etc. in books like Freakonomics and Undercover Economist. The deal was simply I got a free trip in a car ferry to the UK for a car and 2 adults once I completed my trip to Europe. On my return, I phoned and all went perfect. I had to pay a small amount for the kids, but we got the dates we wanted. So how much is this promotion costing the ferry company. I guess there are two ways of looking at it:

1) it costs them the lost revenue from two other paying passengers with a car – so a sort of opportunity cost

2) it costs nil, and in fact increases contribution.

Which one would you use if you were making the decision/reporting to management ? I’d go with the second view, especially in off-season. The ferry in question hardly ever leaves the Irish Sea – going back and forward to the UK three times every 24 hours, all year round. In off-season, the boat is not full – but the costs of running it are the same – both fixed and variable costs. Thus, any extra monies I spend – buying food for example – reduces the fixed costs burden. If I were to think about this free trip in full cost terms, I would probably not offer it to passengers as the fixed cost are unlikely to be covered. This would be the wrong decision in my view, as anything that contributes to the bottom line is better that nothing, or suffering the fixed costs regardless.

Tune in over the coming weeks for some more holiday stories.

A great reporting tool from Excel – PowerMap

As you might know from some of my previous posts, I really like concise presentation of information. The infographic is one of my favourites. Graphical reporting is always great, and managers tend to really like it – it simple, conveys trends, and it’s not boring accounting numbers.

I read a piece on CIMA Insight about a new add-in for Excel 2013 called GeoFlow, or more correctly PowerMap. You can read the full article here. The add-in uses Bing Maps (from Microsoft) and you can plot up to a million rows of data against a map. You can also plot date data, so you could for example see how sales have trended over time on a map. The data can be presented in 3D format, as bubbles, or as a heat map. This tool will certainly create really cool business reports.

Managers should know the numbers

At the end of June this year, Michael O’Leary from Ryanair was his usual self at the Paris Airshow. He let a few jibes fly at almost everyone. He also signed an order with Boeing for new aircraft, worth around $1.5 billion. Plans for future aircraft purchase were mentioned too and O’Leary compared two possible aircraft – one from Boeing and one from Airbus. While he suggested both were similar aircraft, the Boeing has 9 more seats and he said ‘that’s worth a million bucks’. When I read this , I thought is this just another quip or does we know his numbers well?

So, here are my calculations:

9 seats at average revenue of €70 = €630

Assume four flights per day per aircraft, so 630 x 4 =€2,520.

Finally, assume 360 flying days per year, this gives 360 x €2,520 = €907,200.

Let’s not argue over the rounding, and maybe my sums and assumptions are not correct. But a round €1million per aircraft per annum adds up to a lot of money. So although O’Leary’s rule of thumb may seem like a quip, it seems to be quite a good rough measure. He is an accountant after all!

Cash accounting – an alternative to accruals accounting? And what about accounting software?

English: Accounting machine from UK manufacturer Powers-Samas. (Norwegian Technology Museum, Oslo.) (Photo credit: Wikipedia)

In Ireland and the United Kingdom (and maybe come other countries) it has always been possible for smaller business to pay VAT based on cash received rather than on an accruals basis. You probably know what the accruals concept is, but if not click here. When I teach accounting or prepare accounts, the accruals concept is used almost without exception. The profit & loss account (income statement) and balance sheet (statement of financial position) will definitely use the accruals concept. In fact, these financial statement often take a different name and format when prepared for a cash-based business. For example, when I teach how to prepare the financial statement of not-for-profit organisations such as clubs, we often refer to a “Receipts and Payments Account” and a “Statement of Affairs”. The former is like an income statement, but is based on cash records; the latter is a list of assets and liabilities and will normally draw on the accruals concept.

From April 1st 2013, the UK tax authorities permits smaller unincorporated businesses to use a cash based accounting scheme where the turnover is less than £77,000 (see here for more detail). I’m not a UK tax expert, but from my reading about the topic on the web, the “income” of a small business will be the cash received, and the “expenses” will be cash paid for business expenses. This sounds like a reasonable effort to simplify the tax system for the smallest of businesses. The accruals concept may not be that relevant to many of these businesses as, for example, they may have few assets (to depreciate) and receive payment for most work as soon as it is done. So all fine? Well apparently, many accountants protested this new scheme, and that’s not surprising given how the accruals concept is engrained not only in the teaching of accounting, but also in accounting regulations. As a management accountant, I would always encourage the smallest of businesses to think in cash terms – it is easier for business owners with little accounting skills to understand. But I do see one big problem with this scheme in the UK. It centres around what happens when turnover exceeds £77,000. Once this happens, the business must revert to accruals accounting. This would cause much confusion if a business is using accounting software. Normally, accounting software incorporates accruals accounting, but some also support cash accounting in the way described here. I’m not 100% sure, but I would imagine if you set up software to work in one method, it may not be that easy to switch. So even though this cash scheme is easier and optional for small UK business, if they use accounting software (and more and more do) then it is probably best to stick to accruals accounting.

What is activity-based costing?

You may have heard of activity-based costing (or ABC), and here I will try to explain the basics of ABC. First, just a short reminder of the types of cost an organisation may have.

Costs are often classified as fixed or variable. Variable costs change in line with volume/output, and are often called direct costs as they can be attributed easily to a product or service. Fixed costs, often called indirect costs, do not change when business output changes. For example, a fixed cost might be rent of a premises or the salary of a general manager. Such costs cannot be easily traced to a product or service. However, if no effort is made to trace fixed costs to products or services, then the business does not know the full cost. This makes decision-making more difficult.

Traditionally fixed production costs are absorbed into a product by means of a rate per labour hour. For example if overhead was planned at €1 million for a year and 100,000 labour hours were to be worked, then each labour hour would mean a €10 overhead cost. So a product taking two labour hours to make would be charged €20 overhead.

The traditional method can be criticised as over the years more and more overhead has been non-production type overhead and not related to the number of labour hours spent making a product – indeed automation of production in many industries has seen labour being of decreasing importance.

Another more modern way to allocate overhead to products is using ABC. The key in ABC is the word “activity”. In ABC, we can think of an activity as a collection of tasks which are linked in terms of being an overhead cost. For example, customer service, facilities management, quality control and machine setup are all examples of activities. The resources of the activity are determined, which are used to determine the cost of the activity – typically for a year. Then, what causes these resources to increase or decrease is determined. This is called a cost driver. For example, more complaints from customers will increase the resources needed by a customer service department. Using the cost driver, the overhead cost driver rate can be determined. Here’s a brief example:

A design department costs €100,ooo per annum – costs such as salaries, design materials, computer running costs etc. The more designs for new products the greater the cost, this designs are the cost driver. Lets assume there are 5,00o designs per annum, thus the cost driver rate is €20 per design. A product which needs say three designs will thus incur a €60 overhead costs for designs using ABC. If a product has nor designs, then zero overhead is incurred.

In a business, design (as per the above example) may just be one cost driver. Thus, the more resources (activities) consumer by a product the higher the overhead cost. This seems to make a lot of sense, and thus ABC is often used where overhead costs are not easily traced using direct labour hours (or similar) as a means to allocate overhead cost.

With ABC, all direct costs are assigned to the product/service in the same way as traditional costing methods. It is just the allocation of overheads that differs. Typically, ABC considers not only production overhead costs, but many other overhead costs which can be defined within activities.

Related articles

- Two activities for ABC and the appropriate cost drivers for those activities (globalexperts4u.wordpress.com)

- Introducing Overhead Cost (thebangaloresnob.wordpress.com)

Article in MAR – management accounting at Guinness over a century or so

Over the last year or two I have done some research on changes to management accounting practices over a century or so at the Guinness cooperage. This work is now available as a an article in Management Accounting Research see here

CVP in farming

Farmers Market (Photo credit: Macomb Paynes)

As you may know CVP analysis looks at costs, revenues and volumes to determine things like at what output level a business will break even or make a certain profit. This post provides a simple example of the effects of volume on the viability of a business.

Recently, a local authority in Dublin, Ireland announced plans to build a large sewage treatment in the north of the city. As part of this, a vegetable farmer in the area will lose 35 of his 120 or so acres to the plant. I listened to a radio broadcast where the farmer simply said this is too much land to lose and his operation becomes uneconomic.

Let’s think about this briefly in CVP terms. If we assume a stable price for the farmer’s products and stable variable costs (seeds, labour, fuel, fertilisers for example), then it would seem that a loss of about 25% of capacity would reduce the farmer from a profit scenario to a loss one. I am not an agricultural expert, but I would assume that the fixed costs consist largely of the equipment and buildings needed to operate the farm. If the land area is reduced (i.e. capacity is reduced), then the farmer simply does not have enough land left to produce enough revenue to cover these fixed costs and make a profit.

You can read more here.