What is throughput accounting?

Throughput accounting is an alternative to traditional internal cost reporting. It stems from the Theory of Constraints, which I won’t detail here, but essentially this theory suggests an organisational can best achieve its goals (e.g. profit) by maximising it use of a constraining resource. A constraint could be machine capacity for example, and by maximising throughput on the constraint profit is maximised. To report on throughput, a new accounting approach is required, called throughput accounting:

1) Totally variable costs – this means a cost which is incurred only when a product/service is created. This often means only material costs. Labour costs are not totally variable, as employees are typically paid regardless. Some transportation or subcontracting costs may be totally variable. All overhead costs are not totally variable.

2) Throughput – this refers to revenue less totally variable costs. Contribution using throughput accounting is likely to be higher.

3) Operating expenses – this refers to all costs other than totally variable costs. Operating expenses are not distinguished into categories such as fixed or variable, or allocated to products in any way i.e they are similar to period costs, as they are costs which are more

associated with the passage of time than with products.

4) Net profit – in throughput accounting, the net profit is simply throughput minus operating expenses.

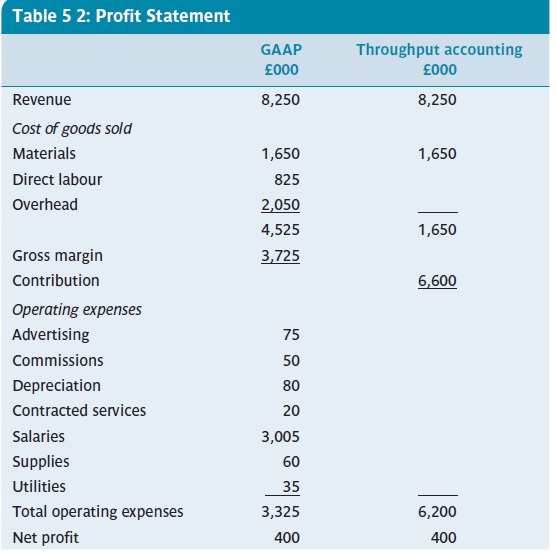

Looking at 1-4 above, you can see no attempt is made to allocate any overhead cost, so throughput accounting does not meet normal GAAP requirements. It does however raise the possibility of selling products/services at a price which is lower than under normal cost accounting, and it may also be useful for short-term decision making. Below is an example of a profit statements from Burns et al (2013. p. 112), which shows how throughput accounting produces a differing view on costing.

The overall net profit figure is exactly the same, but you can see a much bigger contribution under the throughput method. Arguably, as only material costs (in this example) are totally variable, a report such as the one above is very useful for short term decision-making.

References:

Management Accounting, Burns,Quinn, Warren & Oliveira, McGraw-Hill, 2013 – see burnsetal.com

Cost centres – a useful tool in any business

") Managing your business costs and revenues is a challenge. To survive, you have to sell enough products/services, and collect money and manage your costs. The latter can be more difficult than you think, particularly when you don’t have good breakdown of costs.

Managing your business costs and revenues is a challenge. To survive, you have to sell enough products/services, and collect money and manage your costs. The latter can be more difficult than you think, particularly when you don’t have good breakdown of costs.

Without careful monitoring of costs, any business can find that costs can spiral out of control quite rapidly. The old saying “keep an eye on the pennies and the pounds look after themselves” is a good starting point. This does not mean you spend hours and hours monitored costs in minute details, but you should be able to get an overview of all costs at any time. One way to do this is to use cost centres in your accounting system.

What is a cost centre?

A cost centre some section/portion/unit of a business for which costs can be identified and someone is accountable for these cost. Normally, a cost centre has a budget which includes all costs traceable to the cost centre. These cost could be anything from wages to telephone to motor expenses, once they can be traced to the cost centre

In a small business there may be only one or two cost centres. Because you will be looking at small numbers of transactions, there is no need to split things up into smaller cost centres as costs can be more readily monitored against budgeted figures. However, for larger businesses, operating as a single cost centre is probably not good enough. It is also not going to be an easy task to monitor whether those responsible for cost control are doing their job effectively. A breakdown of costs down into each cost centre helps control cost of each cost centre and the business as a whole.

Identifying cost centres

Some businesses are easy to split into individual cost centres – for example, a manufacturing company with six factories, a head office and a distribution warehouse could be split into 6 individual cost centres for each factory), a head office cost centre and a separate distribution cost centre. This example portrays what I call high-level cost centres. A business may need to go into more detail to keep a tighter control of costs – for example, each manufacturing plant might make several different products, with several different machines/processes for each product. It would be possible to treat each machine or process as a costs centre in this case. This would allow the business to keep a good eye of how profitable each product process is. Sometimes too, a business might treat support activities like human resources, finance and logistics as cost centres too. There is no end to how detailed cost centres can be [i.e. they can become very low-level], but remember to be a cost centre, it must be possible to trace costs directly and someone is responsible for the costs.