A management accountant needs to know the business

A fairly obvious title to this post, but it is something we may often forget. As a management accountant you need to know how your business works, and this means getting out to the factory floor, to the process or working with those people doing the necessary tasks.

So why the old tyres Martin you may ask? Well, I recently read a two-page feature in Financial Management on how tyres are made and what happens the old ones – see here. This reminded me of some of my roles in industry. I knew nothing about making clothes or making cardboard when I joined my respective past employers. It is not that I became a technical expert in these areas, but I understood the process, what needed to be done, how the factory worked etc. And how did I learn you may ask? I learned mainly by talking to people, observing how things worked, determining how much things costs, where revenues came from etc. Then, as we updated various systems over the years, my knowledge became deeper and I started to question how some things were done, could they be improved for example. Having read the article in Financial Management, I was thinking based on my experience, if I started to work for a tyre company this would be my day one reading material.

Construction cost management at BER airport

Cost need to be managed. This is term I have probably heard or said many hundreds of times in my life as an accountant and teacher. Managing costs requires two things 1) a knowledge of costs and how costs are structured in the business, project or product and 2) managers. We probably take both of these for granted, but there are some classic examples of when one, other or both do not apply.

If you have ever been involved in a building project, or built your own house, you will know that construction costs are notoriously difficult to manage. Just think of any large building project in your country, was it delivered on time and within budget? Sometimes the answer is yes, but when it is no, it can be a resounding no. Take for example the Berlin airport which is due to be open on 31/10/2020 – probably the worst time in aviation history to open an airport due to the present pandemic. This project started back in 2006, and it is being opened at a cost which is billions in excess of plan. So what went wrong? I could probably write a book about it, but in essence bad management. Of course a large project may be late and over budget, but in the case of Berlin airport, the delay is about a decade and the cost overrun about 3 times. A BBC News article provides a good summary, and I will give some examples. First, there were changes during construction due to plans not including shops for example. This added time and money. Te question has to be how did the “managers” not notice a part of the airport which can give 50% of revenues was not there? Second, there were issues due to there being no specialist contractor, rather many smaller ones who the managers hoped could be compelled to reduce costs. However, not having a single point of contact in a the form of a specialist contractor implied the project management was very complex – and thus costly.

This is just a brief summary. Have a search around to find out more. Here is a nice article on the technical side, or here from CNN – which includes a final cost estimate of €7.3 billion (original plan c. €2 billion)

Photo by Negative Space on Pexels.com

A “living profit”? Some hints from Guinness.

Photo by Engin Akyurt on Pexels.com

A pint of the black stuff (Guinness) would be most enjoyable now, ten weeks into “lockdown”. Of course, this is not a lament to me wanting a pint, but there is link to Guinness.

For quite a few years now, media and commentators have highlighted the large profits and low taxes of many companies. Take amazon.com Inc, whose Q1 sales in 2020 reached $75 billion (see here for more), or think of Apple, Facebook or many other companies. Before I say anything further, I am not a total socialist, nor am I a total capitalist – there is a happy medium in there somewhere. You may know from reading previous posts that I do some historic research on the Guinness company. Dennison and MacDonagh (1998) in their book Guinness 1886-1939: from Incorporation to the Second World War provide some very useful insights into the general management of the company, and I will draw on one of these now.

Sometimes I ask myself why do some companies need to make so much profit? On the other hand, in a democratic/capitalist society, they are free to do so. Now, with a serious pandemic gripping the entire world, some of our underlying models are at least being questioned. So my question is could companies be happy with a “living profit”. I first noticed the term in relation to Guinness dealings with Irish malt suppliers around the turn of the 20th century. The company wished to encourage the production of Irish malt, but were not willing to buy at the lowest market price. Instead the company noted a “living profit” should be attainable. What exactly this means is not specified, but the general principle if clear. Today, most (not all) companies seem to want lowest cost everything and highest profits – presumably to keep shareholders/investors at bay. Would it not be a great improvement for us all if more and more firms took the approach of the “living profit” espoused by Guinness over a century ago? I am sure economists and others could give me many reasons why not. But, perhaps it is worth having the conversation as the business world comes back a new normal in the coming months.

Hand sanitiser instead of gin at Brewdog

As a follow to my last post, have a listen to this podcast from FM Magazine. It’s a similarly interesting story.

Covering costs and ticking over during the pandemic – a nice example

I hope a local distillery near my home does not mind me using their graphic above. As we are all dealing with the effects of the Covid 19 pandemic, I was really impressed to see how small local distilleries in Ireland (and indeed elsewhere and some large ones too) have changed to producing alcohol based hand sanitiser.

Many businesses cannot adapt their products to the current scenario, but the example of distilleries is a really good one. The Listoke Distillery is manufacturing and selling hand sanitiser at cost. Not only is this a good thing for society, it also in my view makes business sense. As the header of this post suggests, it is better to be “ticking over” and covering costs than losing money and not covering fixed costs. I would also bet that many of us (and certainly yours truly) will remember these local small businesses that helped us out in these strange times and, hopefully, they will see increased revenues and growth. Meanwhile, with costs covered, at least they have a good chance of surviving.

By the way, I’ve just bought my second bottle of sanitiser – accompanied by a bottle of gin of course.

The various meanings of cost

If you have studied management accounting, or perhaps read some of my previous posts, you will know the word cost can have many meanings and descriptions. For example, a cost can be fixed, variable, mixed or opportunity.

In this post, I would like to think more about what the word cost can mean outside the world of accounting. The etymology of the word cost is from Latin constare which means to stand firm, stand at a price, which seems to suggest its origins are associated with business transactions. However, today cost can also be used to describe many non- business things. For example, the Alberta oil sands in Canada may have quite a high extraction cost in money terms, but also have and/or will have a large cost in terms of environmental impact.

As I write this post, many of us are working at home due to the global Covid 19 pandemic. This also provides a good example of the many meanings of the word cost. It is perfectly summed up in a phrase I heard on radio “we can count the cost in money now or in more lives lost later”. This comment was in response to plans (or lack of plans) by governments to respond to the pandemic and being more concerned with economic impacts.

These two short examples show cost has meanings which are perhaps commonly understood, and thankfully are becoming more and more a part of business decision-making- which is a good thing of course.

Book value versus market value

Photo by Chad Russell on Pexels.com

A Guardian headline in recent days says “Tesla shares soar 40% after analyst says firm’s value could hit $1.3tn“. Similar headlines could be seen in other newspapers. So, the market values Tesla at $1.3 trillion, yet their 2018 10K shows assets valued at around $30 billion, and accumulated losses of $5.3 billion. So, why are these values so different? This is something students of mine often ask. I’ll try to give a simple answer.

The market value is based on expectations for the future, and these drive up the share price – some media sources though suggest the price is being driven by short sellers trying to buy shares to cover losses they may be making as they bet against Tesla shares rising in price. Accounting values are in general based on historic cost – what was paid for something in the past. Also, for example, accounting does not include items which do not have a historic cost – such as the Tesla brand name. Thus, accounting statements do not reflect future plans or values in general. If another business were to buy Tesla, then its actual (market) values would be captured by accounting of course – brand value, goodwill and such things not captured previously. At this purchase point, there is a historic cost.

Free email is not free.

Telecommunication services in Ireland used to be provided by the State, through various entities. The most recent entity is eircom, now a private firm. eircom were one of the earlier providers of free email accounts, but that is about to change as the company now wish to charge €5.99 per month for email accounts. Well, there is no such thing as a free lunch as the saying goes.

But let’s put on our accounting hats for a minute. There is of course a cost involved in hosting email accounts – servers, cooling, power, buildings. This may have been okay when eircom was a state company and there was less of a profit motive. Gmail is free I hear you say; it is not, you give your data to them to make money from. So eircom probably need to recoup some of their costs, and that seems like a good accounting decision, The price does seem a bit high though – about €4.86 next of VAT will be earned by eircom. To me, it seem more like a prohibitive price, and the real objective to force email account holders to move to other providers.

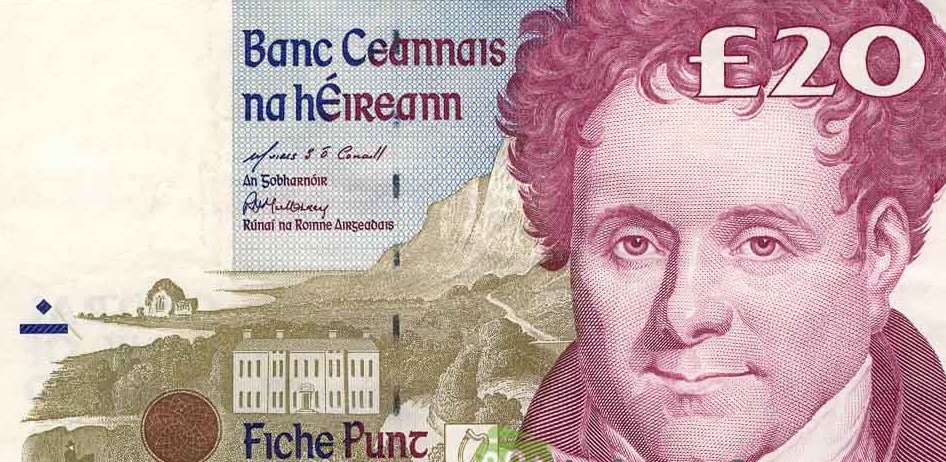

Provisions – an interesting example from a central bank

If you live in Ireland and are of a certain age, you’ll remember the above £20 note, and maybe even the older one with W.B Yeats on it. Now, we have euro notes of course, since 2002. So what if you had old pound notes? Well, when currencies change, there is usually a period of time during which the note can be redeemed at the Central Bank of the country in question. That is exactly the case in Ireland.

So where is the accounting in this you may be thinking? Bank notes have their origin in a “promise to pay the bearer on demand” as it used to say on old Irish currency, and still does on some bank notes. In other words, there is a liability on behalf of a bank to pay something – historically something like “pounds of silver”. In the case of the Irish Central Bank, there is still a liability to repay the the bearers of old currency, namely the Irish pounds. As recently reported, the Irish Central Bank has a provision in its accounts (specifically in the Statement of Financial Position) of €350 million for old notes and coins to be redeemed. This is 18 years after the notes ceased to be in circulation and be legal tender. This is why the term “provision” applies, as according to International Financial Reporting Standards a provision is “a liability of uncertain timing or amount”. In this case of the outstanding old Irish currency, the amount is certain, but the timing is not. I would imagine at some stage, the provision will be reversed, maybe 30 years for example, but until then, it will remain on the books of the Irish Central Bank.

An example of the going concern principle

One of the fundamental accounting concepts is that of going concern. In simple terms, this typically means a business is unlikely to be able to continue in operation for the next 12 months.

It is not very often the examples come to light, but recently in Ireland we had one. The national football association, the Football Association of Ireland, has their auditors state the organisation could not be deemed a going concern. According to the RTÉ news website, the auditors noted:

“While the company has received some advanced funding from UEFA during 2019 to enable the company to meet some of its current liabilities there is not sufficient audit evidence that the company will be able to meet its liabilities as they fall due. Therefore we are unable to obtain sufficient audit evidence to support the assumption that the company will continue as a going concern.”

The piece also notes the levels of debt and losses over several years. The statement above provides a nice clear understanding of what going concern means. Do have a read of the RTÉ article and other coverage to get more insights on the association.

Why do I need to prepare a budget

Photo by Breakingpic on Pexels.com

In my previous post, I mentioned being part of a local voluntary committee, and our efforts to bring a Christmas market to my local town. It’s all going well, but as we near our first year end, it has become apparent to me how important it is for us to plan better for the following year.

Like many voluntary organisations, we are probably still finding our feet. While I keep track of the monies in my role, what I do not have is the full picture of what monies will be spent. To be fair none of us do, as this is the first time we have organised this event and none of us within the organisation have prior experience of such an event. However, a budget is exactly what will bring us together and help us focus for next year. By the end of the Christmas period, we will know what costs we have incurred to host the market and these can be the basis for discussions for the coming year. Then, with a budget in place, we can start to plan for what we need to achieve and of course we can keep a control on things. If you read any management accounting textbook you will see pros and cons of budgeting. To me the biggest advantage of preparing a budget in this small voluntary organisation is that we can all talk from the same page – i.e. the communication value of the budget.

Opportunity costs – lost parking fees

I am a Treasurer on a local committee, whose task it is to bring a Christmas street market to my local town.

We raise sponsorship from local business and in turn the street market will boost Christmas trade it is hoped. Of course to do this, we need the approval of various local authorities, one being our county council. To hold the market, we need permission to close streets, and guess what, there is a small opportunity cost of doing this.

The street has about 15 parking spaces, which are chargeable at a rate of say €1.50 per hour from 08:00 to 18:00. The local council makes the assumption these spaces will be filled – which is probably quite fair – and the have to be paid for the parking revenue lost. This is a classic opportunity cost example, as they lose revenue by granting permission to hold the market, and thus are choosing one option over another. They probably could also add on lost revenues from tickets for illegal parking – I’d be quite sure there are more than one of these each day – but I will keep quiet on that one 🙂

Taiwanese whisk(e)y

Yes, there are some whiskies produced in Taiwan, and they are winning some awards and grabbing attention in the whisky world. I wrote an article on The Conversation recently which looks at how Taiwanese whisky producers have some costs and cashflow advantages over other producers. You can read it here. Sláinte

Photo by Prem Pal Singh on Pexels.com

.

Thomas Cook collapse – breakeven and operation leverage

In the past few days, the Thomas Cook travel company has gone into administration – meaning it’s banks have taken control to recoup monies they have lended. The company dates back to 1841, and is (or was) a well-known brand in the holiday/tour sector.

Of course, here I am interested in the management accounting angle, with a teaching focus. There will no doubt be plenty of comments on the failure, but let others write that. A quote in The Sun (ok not the best source, I acknowledge) noted “the firm has been struggling with a £1.6 billion debt for years. It needs to sell 300 million holidays a year to break even.” I am not sure about the accuracy of the “300 million holidays a year” to break even, but regardless, it is quite likely Thomas Cook would have had to sell a lot of holidays to cover the costs of servicing a large debt (and making repayments) on top of its ongoing costs. What is probably more interesting it the operating leverage within a firm like Thomas Cook.

Operating leverage refers to the percentage of total costs which fixed costs compared to variable costs. If fixed costs are higher in proportion to variable costs, this is referred to as high operating leverage, and more profit is made from each incremental sale. More variable costs, on the other hand, is termed low operating leverage and results in a smaller profit from each incremental sale. Where would Thomas Cook sit on this scale? Well, it likely had high fixed costs (debt servicing, fuel, staff, lease payments on aircraft etc), so is probably on the high operating leverage end of the scale with lots of fixed costs. But, the package holiday (or even the airline sector) is historically a sector with low profit margins. With high fixed costs and low margins, this means a firm like Thomas Cook needed substantial sales volumes and cost controls to keep going (or even break-even) without further funding. It seemed not to be able to do this – 2018 loss after tax was £163m, 2017 profit was £12m, 2016 profit £9m, not great on revenues of about £8 billion.

What is a provision for bad/doubtful debts?

Photo by rawpixel.com on Pexels.com

Back to some basics today, seen as it is almost the beginning of a new academic year for me. I’d like to provide a brief summary of the notion of a provision for bad debts – based on my experience as an accountant mainly, but of course, it is something I would teach too.

First, a provision in accounting is simply an entry for something that has not yet happened but is probable. So, when a business sells on credit, it is likely some portion of customers will not pay – regardless of how good the credit controls are. Thus, based on past experience usually, the accountant in a business will create a provision for bad debts (sometimes called doubtful debts, or irrecoverable debts). At this stage, no specific debt which may be unpaid is identified, it is just a general estimate and the amount is captured as an expense in the income statement of the business. In my experience, the amount set by as a provision in the financial statements is typically about 1-3% of the amount of outstanding receivables, although this can vary from time to time. any adjustments to the amount provided are reflected through the income statement. When a debt is actually identified e.g. a customer goes bankrupt, then this specific amount is a separate expense to the income statement. Such specific debts may cause an accountant to review the amount of the provision too.