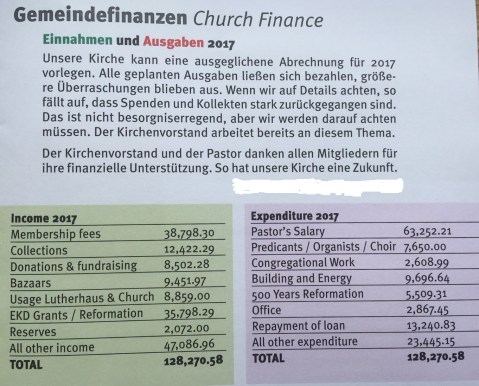

A faulty income statement, or not?

Or a profit and loss account if you like the older term. Below is simple income statement (which has been published in the public domain), or more precisely an income and expense account, which is a term often used in clubs and charities. So, this example if not IFRS based, but the basic principles are the same. To be fair to the preparer of the statement below, it is quite detailed and transparent. But there is one problem – can you spot it? (“Einahment und Ausgaben” could translate as income and expenses or receipts and payments, but I will come back to this below).

Just to remind you, accounts are generally prepared using the accruals concept, but in smaller organisations like churches and charities, using a cash basis is common. Have you spotted what is seemingly incorrect? It is under the “expenditure heading”. Got it? It is the “repayment of loan”. This is a repayment of a capital item, or capital expenditure. Remember that only revenue expenditures appear as expenses in an income statement, so in the case of a loan only the interest on the loan would be included. So is the above statement incorrect? The answer is probably not, but now back to the nuances of language. The statement above is probably best described as a “receipts and payments” account, as it seems to be more representative of cash coming in and going out. We would need to have a chat with the preparer to be sure. However, including the loan repayment is a pointer that the above is not an income statement/profit and loss. This fits too with the nature of the organisation (a church).

You might also notice “reserves” on the income side of the statement above. Again, this is likely a capital item, and maybe should not be included as income. We would need more detail to be sure.

Private companies – what accounting information is available to the public?

As you may know, there are public and private companies. Public companies can sell shares to members of the public, normally through a broker or exchange, private companies cannot. Both must prepare accounts though, and must also file certain accounting information which in turn becomes available to the public. So what accounting data can Joe Blogs get? The answer is it depends, but I will give you a good idea on this post.

In most European countries there is a central register of all companies – as far as I am aware the US does not have such a register, and the SEC focuses on public companies only. In Ireland and the UK, a small fee via an online portal gets me at least a balance sheet of a company – an abridged version for small companies – and an annual return which shows the directors and shareholders and their details (such as address). To give another example, in Germany I can download a free app called the Bundesanzeiger and search for details of any company – again for smaller companies I can get a summarised balance sheet.

For larger companies, including public a lot more information is available of course. But even with a balance sheet, or more of the company is medium or large, I can obtain quite a good picture of the financial position of a private company, and quite detailed information of directors and shareholders. Such information can be very useful to prospective investors, suppliers, customers and even employees. Why not search for a private company you know and see what you can find.