Taiwanese whisk(e)y

Yes, there are some whiskies produced in Taiwan, and they are winning some awards and grabbing attention in the whisky world. I wrote an article on The Conversation recently which looks at how Taiwanese whisky producers have some costs and cashflow advantages over other producers. You can read it here. Sláinte

Photo by Prem Pal Singh on Pexels.com

.

Thomas Cook collapse – breakeven and operation leverage

In the past few days, the Thomas Cook travel company has gone into administration – meaning it’s banks have taken control to recoup monies they have lended. The company dates back to 1841, and is (or was) a well-known brand in the holiday/tour sector.

Of course, here I am interested in the management accounting angle, with a teaching focus. There will no doubt be plenty of comments on the failure, but let others write that. A quote in The Sun (ok not the best source, I acknowledge) noted “the firm has been struggling with a £1.6 billion debt for years. It needs to sell 300 million holidays a year to break even.” I am not sure about the accuracy of the “300 million holidays a year” to break even, but regardless, it is quite likely Thomas Cook would have had to sell a lot of holidays to cover the costs of servicing a large debt (and making repayments) on top of its ongoing costs. What is probably more interesting it the operating leverage within a firm like Thomas Cook.

Operating leverage refers to the percentage of total costs which fixed costs compared to variable costs. If fixed costs are higher in proportion to variable costs, this is referred to as high operating leverage, and more profit is made from each incremental sale. More variable costs, on the other hand, is termed low operating leverage and results in a smaller profit from each incremental sale. Where would Thomas Cook sit on this scale? Well, it likely had high fixed costs (debt servicing, fuel, staff, lease payments on aircraft etc), so is probably on the high operating leverage end of the scale with lots of fixed costs. But, the package holiday (or even the airline sector) is historically a sector with low profit margins. With high fixed costs and low margins, this means a firm like Thomas Cook needed substantial sales volumes and cost controls to keep going (or even break-even) without further funding. It seemed not to be able to do this – 2018 loss after tax was £163m, 2017 profit was £12m, 2016 profit £9m, not great on revenues of about £8 billion.

The “cost” of refunds and claims – a management accounting view.

In recent years in Ireland, business insurance costs have been increased dramatically due to increasing volumes of claims against them. In some cases, the costs have increased so much that the businesses have simply closed. This post is more about the smaller claims, claims for refunds or costs incurred because a product or service was not up to scratch.

I will use Ryanair as the example here. Despite all the criticisms levelled against it, it remains one of my favourite airlines. They run a tight operation and keep costs to a minimum. They also do not payout refunds or claims unless they have to, this is the fun part for me. In a recent Irish Times article, there are details of a customer claiming €222 for taxi fares incurred due to a Ryanair mistake. The company fought it, but the passenger pursued through a small claims court and got their money refunded. Fair play to the passenger.

Recently I was subject to a delay on a Ryanair flight from Bristol. Some passengers, those who were UK citizens I later found out, were offered £5 refreshment vouchers. I was not, and followed up. To be fair to Ryanair they said if I could produce a receipt, they would refund me.

Now the accounting part. In both examples above there are a lot of costs already incurred in having a customer service function to deal with such issues. Let’s deem these as sunk costs. Once a claim is initiated, then I think we could see the situation as an instance of activity based costing perhaps. In my own case, I sent three emails and I can guarantee the cost of dealing with me was way more that the price of a cup of coffee I was seeking to claim. In the case of the passenger taxi fares, costs of engaging solicitors by Ryanair would have far exceeded the cost of the refund had they simply paid it based on the passengers receipts.

The point I am trying to make is that while I fully agree that firms should not just pay refunds without any basis, there is likely some value at which it costs more to defend a refund claim than simply pay it – with vouched receipts of course, not like me and my coffee. But, if you are not getting satisfaction from a company if you feel you should get a refund, apart from legal options, you can always waste their time a little and get some satisfaction that way.

Reasonable business expenses

I am sure you have read or heard stories in your country about political leaders or CEOs spending large amounts of money on expenses – hotels, meals etc. I have read a lot of such reports in recent weeks and just wanted to give a view on it.

To me, and much of this is based on experience, the first principle to me is simple – no receipt or invoice, then any expense should not be reimbursed. Doing this sets a basic principle which is easily understood. I have heard some comments over the years that there is a cost is running an expenses reimbursement system, which may exceed the value of the expenses, so why bother. This may be true in some cases, but I do not agree.

A second principle to me is a basic accounting one – business expenses only. The idea of say using a business credit card for personal lunches or whatever at a weekend goes against the entity principle. This principle means only items for the business should no part of the accounting for that business.

Third, the expense, once for the entity should be reasonable, but what is reasonable? This is where common sense must apply. Let’s take hotels as an example. It may be that a room for €100 per night is ample for any business person, but in some cities this may not be enough for even a basic hotel. But, if I were to say €1000 per night, you would probably think that is a bit too much. Of course you may have read reports of business leaders and political figures spending many thousands of Euro/Pounds/Dollars per night on hotels. Is this reasonable? Personally I do think some of these people could be a bit more modest!

Costs of the Irish president

The gentleman above is Michael D Higgins, the Irish president – of course he is well known to me and other Irish people, but just for the benefit for others you might read my blog.

The gentleman above is Michael D Higgins, the Irish president – of course he is well known to me and other Irish people, but just for the benefit for others you might read my blog.

In October, there will be a presidential election and Michael D is up for a second term of office most likely. In recent months there has been a lot of media attention as of how much the presidential office costs to run. The office does not have much power, but is a great representation of Ireland as a country. According to the presidential website, the cost is about €3.6 million per annum. The vast majority of this consists of staff and travel costs. However, in various media outlets I have heard numbers being mentioned about the costs of the police officers and army associated with the presidential office. At the link above, these count for about €250,000 in 2017.

So what you say! Well, are these costs relevant to the cost of the presidential office? Would they be avoided if the office ceased to be? I doubt it, as the army and police would be put back to their normal duties. So this is a simple example of costs not bring relevant, and thus they probably should be excluded from any comments or analysis. I would guess too that the kind of simple analysis I have done here might be applied to many other political figures. What is probably most important though is that the costs of the office of the Irish president are now being discussed and new controls and checks may result – which is a good thing.

A quick lesson on blockchain for accountants: Part 2 – mining cryptocurrency

In Part 1 two weeks ago, I wrote about currency. Here, I’ll explain how “miners” help a cryptocurrency like bitcoin be useable.

In Part 1 two weeks ago, I wrote about currency. Here, I’ll explain how “miners” help a cryptocurrency like bitcoin be useable.

To be honest, I had no idea until recently what bitcoin mining actually means – and remember bitcoin is just one cryptocurrency, but I will use it here as an example.

Some weeks ago, I visited a friend of mine who owns and runs a technology maintenance firm. His office is always full of various parts of computers, but on this visit I noticed the office was quite warm and there was a hum of computer fans. So, I stuck my head around a corner and I seen something like what is in the picture above. So, joking I said, “what are you at now, mining bitcoin?”. “Yep” was the reply. So I took the opportunity to lean on my friend for some explanations.

The bottom line for me as an accountant, is that a “bit-coin mining rig” like that in the photo costs about €3,000 and can earn about €500 per month before energy costs – I will come back to these costs in a later post. So what the hell is it and what does it do I hear you ask? In my previous post, I established that bitcoin is not really a currency (yet) in the sense of dollars, euro or pounds. It also does not have a central bank behind it, or commercial banks taking it on board as a major currency. So this creates a problem, which in essence is if I want to pay you one bitcoin, how is this to be done – and remember bitcoin is an electronic medium, there are no paper notes.

Well, if I were to pay for a coffee with my credit/debit card, there is an extensive payments processing system behind the payment – think of the credit card machine, Visa/Mastercard/Amex systems and ultimately the retailer’s bank. Also, you may know that for every card transaction, the retailer is charged by the bank so they never get the full value of a card sale. For a bitcoin payment, where is the system? This is where the “miners” come in. A miner is someone who essentially processes bitcoin payments. My friend mentioned above told me the steps roughly are as follows:

- you get a rig (like the picture above). The faster the better, so rigs tend to use the fastest available memory cards – think about the graphics in a gaming console – these use really fast memory.

- Join a mining community

- Start solving hashes (encryption puzzles)- that is, process and verify bitcoin transactions. This includes working with blockchain, which will be explained in an upcoming post.

- Get a commission for each transaction

- Transfer the commission to a bitcoin wallet – for example, the Coinbase app

- Transfer to your bank account as you see fit.

So, in essence, a bitcoin miner like my friend is taking the place of the commercial banks and/or credit companies and processing payments. It is basically a form of distributed computing.

So from an accounting perspective what does this mean? Well, not very much actually. But, and this is a big but, would/could we trust people like my friend to effectively become a banking system. Personally, I am not sure. We have decades of regulation around our banking systems, and even with all the oversight, it still fails from time to time. The counter-argument could be something like the redundancy of systems or devolvement of the now rather central power of the banking and finance systems. But I’m not so sure just yet.

My next post will explain the basics of encryption.

Activity-based costing in healthcare

Photo by Pixabay on Pexels.com

When I teach Activity-based costing (ABC), one of the example sectors often given to students is healthcare. Just in case you don’t know, ABC is a costing technique which allocates cost to products or services based on resources used by the product or service. If you think about healthcare, even in a standard medical procedure, no two patients are the same and use more or less drugs, time, hospital resources etc. Thus ABC appears useful – one patient may use more resources than the other and so cost more.

Of course, healthcare systems around the world vary. Some are fully funded by taxation, some are fully private. In Ireland, the system is mainly a public one, but unfortunately, it is not great in terms of access to treatment. So, if you can afford it, you can have private medical insurance (US style, but less costly) and this gives you more options. With this in mind, here is my recent experience which made me think about ABC and write this post.

Last year, I spent 11 days in a hospital for some heart surgery. Thankfully all is well. I am lucky enough to have health insurance. About three months post-surgery, I received an advice from my insurer stating how much the hospital had been paid – about €25,000. Phew, thankfully I did not have to find the cash for that! The advice was interesting in that showed little sign of ABC techniques – and as my hospital was one of the more advanced and modern I would have expected it to use ABC, to be honest. What the advice showed was a charge per day, with this charge being higher for two days in intensive care. Otherwise, there is little else. Unfortunately for me, I had some complications which required more drugs and attention from staff, so I took up more time and resources than some of my hospital mates (trust me, you make some good friends in hospitals). But this is not reflected in the cost. I suppose on balance things work out for the hospital and it may not matter, but to me, this simple example is a prime case where ABC could be used easily. If it were, then maybe health insurance costs would be a lot less in some cases – but that’s a whole other debate.

Having said all of the above, research on ABC use shows it is often less than 20% in practice. So maybe I should not be expecting its use in my hospital at all.

The cost of medicines – a quick view

I’ve been quiet recently on here due to some illness. While I’ll and having some time on my hands I began to ponder the cost of medicine and where I live ( Ireland ). I know we are one of the more expensive places to buy medicine in Europe, but here I’m not going to refer to any price indices or similar. Instead I’m going to try to quickly break down the costs of doing business in two countries – Ireland and Spain – to explain price differences. A business manager might do this regularly to gauge the competition. To give an example of the price difference, I know that a common prescription pain killer costs €26 in Spain versus €42 in Ireland. Some medicine I use myself costs about €12, versus €23 in Spain. And just tonne clear, these two examples are for identical nongeneric medicines.

The first is taxes. I found that most medicines in Spain have 4% VAT, whereas most in Ireland are at 0%. So we can rule this out. Second, a tax consultant in Spain told me that to purchase a pharmacy in the city I stayed in would cost about €2 million. This is due to limits on how many pharmacy licences there are. This cost results in high depreciation from an accounting perspective, and is similar to Ireland. Third, by my guess, all other costs like labour, rent, light etc are cheaper in Spain, probably 10-50% less. So this leads me to one remaining thing – profit margins. The profit margin would be spit between the pharmaceutical company, a distributor and the pharmacy itself. Without insider information, it is very hard to know what these margins are. Having said that, they must be a large explanatory factor for the price difference.

And for the fun, to give a more marked price difference. I recently saw a TV programme on the cost of medicine in the US. It not the cost of a monthly supply of insulin at $900. This was quite unaffordable for pensioners on a low income. Many who are near the Canadian borders drive across to Canada, where the price of the same product is CAD$ 120.

Of course, I’m doing a quick and dirty, non- scientific analysis here. But business is full of gut instinct and similar, and my experience and gut tells me profit margins are a huge explainer for medicine price differences between countries.

Food supply chain and accounting

In my daily work as an accounting academic, income across many papers and articles which explore the broader role of accounting in society and out daily lives. Lisa Jack from the University of Portsmouth writes about the role of accounting in the food supply chain. This is a very interesting area, as information on costs and margins is crucial in the food sector. She has just published an article on the recent contamination of eggs in some

European countries – you can read it here. It gives a good overview of how accounting is entwined in this and other food issues, and how it could help.

Understanding costs is key

I probably don’t need to explain the title of this short post, it’s quite obvious. Any business needs to appreciate all costs of the products or services it delivers.

- In past years, manufacturing has shifted to some degree to lower cost locations such as China, and the Foxconn relationship with Apple is a classic case. In the case of a product like an iPhone or iPad, it’s quite easy to see how the assembly costs are probably the higher component, and as they are small, distribution costs are low. But as a recent article in Forbes shows, transport costs are often a reason for manufacturing being close to market. In the article, there is mention of Foxconn planning to $10 billion plant in the US to build larger displays – for say 60 inch TVs. The article notes that the cost of capital in the US is similar to anywhere else, and labour costs and relatively low, although higher than China. However, the transportation costs would be much lower for such larger displays and thus it makes sense to build a new plant in the US.

Bad PR and avoidable costs at United Airlines

Image from Bloomberg.com

Recently, it seems United Airlines got themselves into a bit of a bad public relations scenario by ejecting passengers (with force) from a domestic US flight. I’ve never used United and based in this, I never will, as it seems they commonly overbook flights.

First, in the age of technology we live in, how the hell a system allows overbooking I cannot fathom. Maybe if a smaller replacement aircraft transpired in an emergency, I can understand, but this would not be an overbooking issue.

You can read an article about the event at the link above, but here’s a brief rundown:

- United over book

- They look for four volunteers

- They offer $400, then $800

- Nobody volunteers

- They forcibly remove four passengers

And all of this to get their own crew to a location for the next day – this alone says a lot about their ability to manage the business, not having a standard way to get staff, or reserving x seats for staff.

Back to management accounting, and we know that an avoidable cost is one which can be eliminated by not doing something e.g. close a production line. We also know that in the long term, all costs are avoidable. So what about the United story. Well, one thing that will no doubt happen is a string of expensive law suits – and I personally hope United get screwed. This is an avoidable cost, and surely are the costs associated with the apparent regular overbooking. I’d even have a wild guess that it may have been cheaper to charter an aircraft for the staff than what this will ultimately cost United. Even $5000 a passenger to entice volunteers would be cheap too, or maybe $50000. Regardless, United need to find a long term solution to avoid such costs. They have apparently now increased the offer to passengers to $10,000 to give to give up their seats.

Getting paid – it’s a must for any organisation, even the HSE

The Health Service Executive (HSE) is responsible for Ireland’s public health service. It has been the subject to criticism over the years for being inefficient and it is one of the largest items of public expenditure.

The Health Service Executive (HSE) is responsible for Ireland’s public health service. It has been the subject to criticism over the years for being inefficient and it is one of the largest items of public expenditure.

Thankfully, I have not been a frequent user of HSE services – that is, I have been generally healthy. My son had a mild concussion recently, so we had to attend the A &E department in our local hospital. On attending A & E, every patient is charged €100. The idea of this fee is two-fold 1) to stop the use of A & E by people with non-urgent issues and 2) to help reduce budgetary cost pressures. Both of these are fine in my view.

So, good law-abiding citizens as we are, we asked to pay as we entered. We were told “come back when you leave”. So we did, and were told “we’ll post the invoice”. So now, reflecting on this as an accountant, that’s two opportunities missed to collect payment. Then we get the invoice. There is no bank account details on it, and I cannot pay online. I have to call a number which was always busy. I could pay at a Post Office – fine if I am not working or have one close to work – I do work and I don’t have one close. Eventually we paid! If I do a quick media search I can find one hospital owed €600,000, and some reports from a few years back suggest the HSE are owed €200m . Apparently, people who do not pay are pursued, but how much does this cost? A lot more than the amount collected perhaps, which is not good for a cost stretched organisation.

To me, the process of payment should be much easier. Twice we asked at the hospital. I did not check if they had a credit card machine there, but why would they not. Why can I not pay online or to a bank account, or by PayPal? I shared my story with some friends, and they tell me some hospitals accept online payment. This made me even more annoyed, not even a common system! The lesson here is, and it applies to all businesses and organisations, you have to collect monies owed. The first thing then is to make it easy to pay, and to me the HSE fails badly in this regard.

Storytelling and numbers

Everyone loves a good story. But should accountants tell stories? Here is great post I found in LinkedIn which shows the value of stories

Everyone loves a good story. But should accountants tell stories? Here is great post I found in LinkedIn which shows the value of stories

The better accountants????

This blog post appeared in my LinkedIn recently. Have a read. It’s basically claiming that British accountants are worse than their American counterparts because they don’t use technology as much as. Now, I’m a big fan of technology, but I’m also old enough to have worked before the internet and all other things which make our life easier (supposedly). The author of the blog should know that all technology is a series of instructions in some or other code, and that code is only as good as the person writing it! We are becoming way too reliant on technology and it’s no harm to do it the old way, or use less technology from time to time. If I were recruiting an accountant tomorrow, while their grasp of technology would be something I’d look out for, it’s not the only thing.

And to end, Irish accountants are best 😀

Some insights from IAG

IAG, or the International Airlines Group, is the the parent of Aer Lingus, British Airways and Iberia. In my university, we were lucky enough to have their CEO, Willie Walsh, speak to us before Christmas.

IAG, or the International Airlines Group, is the the parent of Aer Lingus, British Airways and Iberia. In my university, we were lucky enough to have their CEO, Willie Walsh, speak to us before Christmas.

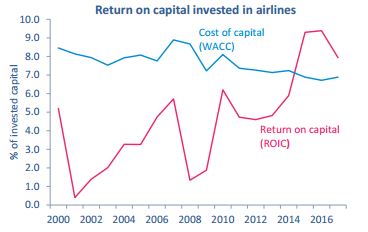

Some things he mentioned are relevant to this blog, and of course interesting. One thing Mr Walsh noted was how only in recent years has the airline sector actually made a return on capital. This must be attributable in some way to a focus on cost by the sector in recent years. The chart below from IATA shows what I mean. As you can see, the cost of capital was higher than the return until 2014.

As my last post indicated, a focus on cost and efficiency has been a feature of the airline sector in recent years. To give another example, Mr Walsh cited an example of using two larger aircraft on a route without a loss in passenger capacity. So fuel, crew and capital cost all decrease in such a scenario. In addition, it freed up a slot at London’s Heathrow airport, which can then be used to generate more revenues.